Researchers at the San Raffaele Telethon Institute for Gene Therapy (SR-Tiget) in Italy have developed a gene editing platform they say improves the precision and safety of CRISPR-Cas9 gene editing in human hematopoietic stem and progenitor cells (HSPCs), a development that addresses the long-standing difficulty of ensuring that edited stem cells carry only the intended genetic change without unintended genomic alterations. Details of the new platform, called SMArT (Selection by Means of Artificial Transactivators), are published in Nature Biotechnology.

“These unintended outcomes, such as large deletions of DNA sequences, have emerged as one of the most important limitations to the broader application of gene editing, especially in stem cells intended for transplantation,” said senior author Luigi Naldini, MD, PhD, director of SR-Tiget. “With SMArT, we aimed to create an intelligent selection system capable of identifying and enriching only those cells that achieved the desired genetic correction while excluding cells carrying potentially dangerous alterations.”

CRISPR-based therapies such as exagamglogene autotemcel (Casgevy) have already reached regulatory approval for hemoglobinopathies, the vanguard of the expected wave of CRISPR-based gene therapies. But drugs like Casgevy use CRISPR to knock out the disease causing gene, while approaches aimed at creating homology-directed repair (HDR), whereby a gene is inserted have been plagued by unintended genetic changes at the editing site. To date, HDR has been constrained by cell cycle limitations and competing DNA repair pathways that can generate deletions, rearrangements, and other structural changes at the target location.

SMArT was developed to address both low HDR efficiency and the unintended heterogeneity of the gene editing approaches. To do this the investigators created a method whereby transient synthetic “AND-gate” circuits are activated only when two conditions are met: successful targeted integration of a gene-sized cassette and preservation of correct genomic architecture at the edited locus. Only these cells transiently express a selectable marker, enabling their enrichment while removing cells carrying aberrant edits.

“HDR-edited HSPCs were enriched to 80–100% purity through transient selector expression, whereas cells carrying undesired and potentially genotoxic on-target edits were preferentially depleted,” the researchers wrote. They also showed that after transplantation into immunodeficient mice, the enriched cells sustained long-term human hematopoiesis, and the selector system was no longer detectable.

SMArT was developed in three configurations SMArT-1, SMArT-2, and SMArT-3. The most advanced version, SMArT-3, employs a CRISPR-based regulatory architecture that can detect correct integration of the edit at the intended site while also transiently activating genes to support stem cell engraftment. One version of this system uses a single programmable CRISPR-based regulatory system to reduce the need for multiple components.

In preclinical models, SMArT was tested in human HSPCs targeting loci relevant to inherited immune disorders, including X-linked severe combined immunodeficiency (SCID-X1) and Hyper-IgM syndrome. The system successfully enriched for correctly edited cells while reducing large deletions and other structural abnormalities associated with CRISPR-induced DNA repair. The selected cells demonstrated multilineage differentiation capacity after engraftment in mice, exhibiting preserved stem cell function.

“Our goal was not simply to improve editing efficiency, but to fundamentally rethink how to control the quality of edited cell products,” said co-senior author Samuele Ferrari, PhD, a project leader at SR-Tiget. “SMArT introduces a programmable framework that can simultaneously increase precision, reduce genotoxic burden, and preserve the functional potential of stem cells.”

The researcher noted that the SMArT platform is designed to be usable across loci and compatible with other genome engineering technologies beyond CRISPR-Cas9, including emerging targeted integration systems. The also believe it can be used to address multiple genetic diseases, particularly those requiring durable correction of blood or immune cell lineages.

Next steps include improving manufacturing efficiency, preserving clonal diversity during selection, and optimizing delivery methods for HDR templates. SMArT will also need evaluation to determine how it performs across different disease contexts and stem cell sources, as well as how it may integrate with non-myeloablative conditioning approaches to therapeutic development.

High-resolution extracellular electrophysiology is typically used to record from neurons in order to understand brain function. Combining electrophysiology with optogenetics allows researchers to test the causal role of specific neurons by activating or inactivating those populations while recording the effects of neural activity.

Now, a new technology, co-developed by UCL scientists, simultaneously records and manipulates neuronal activity deep within the brain. The device, known as Neuropixels Opto and researched in mice, integrates electrophysiology and optogenetics in a single probe, enabling unprecedented insight into how individual neurons in the brain function and interact. By packing around 1,000 closely spaced recording sites onto an ultra-thin probe, it is possible to capture high-resolution signals from individual brain cells while monitoring large neural networks at the same time. The device could transform our understanding of neural circuits and neurological conditions, such as Alzheimer’s disease and schizophrenia.

“This makes it possible, for the first time, to directly test how specific neurons influence the activity of surrounding circuits—revealing causal relationships between neuronal activity and brain function,” notes Matteo Carandini, PhD, a professor at the UCL Institute of Ophthalmology. “The ability to both record and control neuronal activity in the same experiment represents a significant advance for neuroscience.”

This work is published in Nature Methods in the paper, “Neuropixels Opto: combining high-resolution electrophysiology and optogenetics.” The device, which packs 960 electrical recording sites and two sets of 14 light emitters onto a 70-μm-wide, 1-cm-long shank, allows spatially addressable optogenetic stimulation with blue and red light. The device allows researchers to monitor the electrical activity of hundreds of neurons while also selectively activating or silencing specific cells using light.

“The brain processes information through complex patterns of electrical activity, with billions of neurons communicating via rapid electrical signals,” explains Carandini. “Understanding how these signals give rise to behavior, thought and disease requires tools that can both observe and influence neuronal activity.”

“Until now, scientists have typically relied on separate approaches: electrophysiological probes to record neural activity, and optogenetics to control it,” Carandini adds. “Combining the two has proved challenging, particularly in deeper brain regions, where delivering light without disrupting sensitive recordings is technically difficult. Neuropixels Opto overcomes these limitations by integrating both capabilities into a single device, enabling simultaneous measurement and manipulation of neural circuits.”

Karolina Socha, PhD, research fellow at UCL Institute of Ophthalmology, has used the probes to investigate the function of the cerebral cortex. “We were surprised to discover that the activity of neurons in the cortex can be remarkably localized. Up to now, we thought that neurons are so interconnected that there would be no way to activate some of them without activating many others,” she said. “The new Neuropixels Opto probes revealed that these neurons can operate not only in concert but also rather independently.”

The technology may also have important implications for understanding neurological and psychiatric conditions. Many disorders, including schizophrenia, Alzheimer’s Disease and Parkinson’s Disease, are associated with disruptions in how neurons communicate. By providing a clearer picture of how neural circuits function in both healthy and diseased states, Neuropixels Opto could support the development of more targeted treatments.

Revolution Medicines reports that its investigational drug daraxonrasib doubled the overall survival of patients with metastatic pancreatic cancer compared to standard chemotherapy, according to results from the Phase III RASolute 302 trial. These findings were published yesterday in The New England Journal of Medicine and presented at the 2026 American Society of Clinical Oncology (ASCO) Annual Meeting.

“In this trial, daraxonrasib redefined treatment expectations in previously treated metastatic pancreatic cancer by reducing the risk of death by 60% and increasing median overall survival to more than one year, a result not previously reported in any Phase III clinical trial in any line of therapy for this disease,” said Mark A. Goldsmith, MD, PhD, chief executive officer and chairman of Revolution Medicines.

Pancreatic ductal adenocarcinoma (PDAC) is one of the deadliest cancer diagnoses, with a five-year survival rate of 3%. Currently available therapies offer very limited benefits for these patients, especially for those who have already been treated with a first line of chemotherapy and continued to see tumor progression.

In over 90% of pancreatic tumors, mutations that result in an overactivation of RAS(ON) signaling are a major driver of cancer growth. Daraxonrasib is an oral drug designed to block a broad spectrum of wild type and mutant RAS variants. The RASolute 302 trial set out to compare the effects of a daily dose of daraxonrasib to a standard chemotherapy course in 500 patients with metastatic pancreatic cancer who had previously received a first line of chemotherapy.

Results show that daraxonrasib increased the median overall survival from 6.6 to 13.2 months, while boosting progression-free survival from 3.5 to 7.3 months. Notably, these effects were consistent regardless of whether the tumors carried RAS mutations. Serious side effects were reported less frequently by patients who received daraxonrasib, reducing the likelihood of a patient having to discontinue treatment due to side effects by 10 times.

“Daraxonrasib significantly elevates the survival bar in the treatment of one of the deadliest human cancers, while better preserving quality of life compared to chemotherapy,” said Goldsmith. “These striking results firmly support daraxonrasib as the new standard of care for patients with previously treated metastatic pancreatic cancer, and usher in a new era of RAS-targeted therapy for patients living with this disease.”

Revolution Medicines has stated its intention to submit this data to the FDA and other regulators to seek approval of daraxonrasib in this patient population. Three other Phase III trials are currently underway, evaluating the drug in patients with PDAC and metastatic non-small cell lung cancer.

“These results from the Phase III RASolute 302 trial of daraxonrasib represent a major milestone for patients facing metastatic pancreatic cancer,” said Brian M. Wolpin, MD, director of the Hale Family Center for Pancreatic Cancer Research at the Dana-Farber Cancer Institute, professor of medicine at Harvard Medical School, and principal investigator for the RASolute 302 trial.

“For many patients, second line chemotherapy provides modest benefits, and new treatments delivering more durable tumor control have been urgently needed. These results will change how scientists, clinicians, and patients think about treatment for pancreatic cancer, and support a new paradigm where RAS(ON) inhibition enters standard of care for patients with previously treated metastatic pancreatic adenocarcinoma.”

The 2030 patent cliff may either decimate revenue streams or provide an opportunity for innovation that can transform the biopharmaceutical industry. As it stands today, some 200 biopharmaceuticals are scheduled to go off patent during the next four years, representing approximately $300 billion in revenue.

That revenue hit can be softened if biopharma manufacturers replace traditional mammalian expression systems with a Lemna plant-based system. Susan Stipa, CEO and co-founder of Phylloceuticals, tells GEN the Lemna platform her team has developed can reduce operational costs by nearly 80%–90% per gram in the upstream part of the process and one-third the cost overall. That’s because Lemna-based production lacks the 12-month lag and need for sterile growth media associated with mammalian cell lines and has less need for viral deactivation.

Demonstrating those points, Phylloceuticals’ Lemna-based approach produced microgram quantities of the PD-1 inhibitor pembrolizumab in only 16 weeks. Batch harvesting garnered “yields of approximately 0.6 grams purified mAb per kilogram of fresh weight,” Stipa says.

This isn’t how production has been traditionally handled, she says. So, “most companies are making defensive plays—such as mergers and acquisitions, reformulations, and reducing headcounts. But…what if the patent cliff could be an opportunity?”

The duckweed advantage

In optimal conditions Lemna, a genus of small free-floating aquatic flowering plants also known as duckweed, can double within 36 hours. In the wild, five to seven days is normal. “It’s one of the most prolific plants in the world,” Stipa points out. That rapid doubling time creates a huge speed advantage for line development and scale-up. “Line development speed for Lemna is four to six months versus 18+ months for Chinese hamster ovaries (CHO) cells,” Stipa says, “primarily due to Lemna’s genetic stability and clonal growth.” It boasts inexpensive, animal serum-free growth medium, no adventitious viruses, a negative carbon footprint, and uses about 10% of the water used by CHO cell systems to produce mAbs. And, she adds, “There is near-zero impact from unforeseen environmental deviations, like power outages.”

Susan Stipa CEO, Co-Founder

Importantly, “As a multicellular eukaryote, it possesses the advanced chaperones and complex post-translational modification machinery—specifically sophisticated N-glycosylation—required to correctly fold and stabilize large, bioactive human molecules. Our ability with duckweed to control sugars and, in particular, obtain human (or human-like) sugar profiles is what sets us apart.”

Those features make Lemna an attractive alternative to the more expensive CHO and other mammalian cell lines. CHO cells require a very complex system, and “thousands of CHO cells must be screened to find the cell that produces the right protein and remains genetically stable. There can be genetic drift, but with Lemna, there is none,” Stipa points out. Mammalian cells are sensitive to environmental fluctuations and require skilled technicians to manage them.

“Almost anything you can make in mammalian cells, you can make in duckweed, just a little bit better. And, yes, we do a bit better with folding,” she says.

Yeast such as Pichia pastoris or Saccharomyces cerevisiae is another option, but Stipa points out, “Yeast is a story of quantity versus quality. It can produce a lot very quickly, and it does simple proteins very well, but when the protein size and complexity increase, productivity drops.”

Building where there’s a need

That said, Phylloceuticalshas a potentially broad client base that includes individual investigators needing microgram quantities up to contract development organizations, biosimilar manufacturers, and innovators. The company is still young, though. “We need to prove the platform is what the industry wants it to be,” Stipa says.

Stipa developed a comprehensive view of the industry as a young cancer patient and through a career as a chemical process engineer who built biopharma facilities globally, and as a life sciences marketer exposed to many companies.

Her time in marketing, in fact, led to the formation of Phylloceuticals. “I had developed brand strategy for so many start-ups only to see the scientist-founders lose the room pretty quickly,” Stipa says. “In today’s media-saturated world, innovative science also needs advocates able to tell incredibly compelling stories, and to tell them so they stick.”

In 2024, Stipa and her co-founders, Lynn Dickey, PhD, now chief technology and science officer, and Bill Brydges, one of the original leaders of bioengineering firm Foster-Wheeler Biokinetics, incorporated Phylloceuticals.

The company became operational in January 2025, opening its pilot facility in Rapid City, South Dakota. “Our location choice perfectly mirrors the bio-agility of our platform,” Stipa says. “Traditional mammalian cell [production facilities] are often tied to very specific legacy pharma hubs. The idea of Phylloceuticals is that we can be up and running anywhere the need is, and in underserved regions. Rapid City is at the core of one of the largest rural healthcare areas [in the U.S.].”

That the facility was operational in only 12 weeks helped Phylloceuticals transition from friends and family financing to angel investment. Stipa says she expects to close the company’s first funding round soon, “to be followed immediately by a Series A round.”

Initial focus: biosimilars

The company’s focus on biosimilars is directly related to the patent cliff and the industry’s widely discussed onshoring. The COVID pandemic highlighted a flaw in the global supply chain that left nations dependent upon others for critical pharmaceutical ingredients. Plugging that gap with the Biosecure Act (signed into law December 2025) and Federal Acquisition Regulations that ban commerce with companies of concern, Stipa says, makes Phylloceuticals an attractive choice for low-cost, onshore, mAb production. “Beyond biosimilars, we are also very active in animal health biologics and ADC/RTL support,” she adds.

Regulators—notably the FDA—are familiar with Lemna because of its commercial-scale use for food, and for pharmaceutical products that have been through Phase II, including β-interferon, although it hasn’t been used commercially for pharmaceutical products. Commercial scale has been on Stipa’s mind since the beginning. “From the very early months, we had a team beginning to think about what scale-up would look like. Even when we didn’t have the funds, we had advisors working on the scaleup question,” Stipa says. Currently, Phylloceuticals can make microgram-to-gram quantities. Its next phase is to make gram-to-kilogram quantities.

Challenges

“I think pharma rarely fails because of the science,” Stipa says. She says the company is still improving extraction from the apoplast (the network of cell walls and intercellular spaces that help transport water and nutrients) and scaling to commercial quantities.

Instead, the big challenge for Phylloceuticals is simply innovating in an industry that has a legacy, multi-billion-dollar investment in stainless steel infrastructure. “Change is hard,” she acknowledges. But change is also inevitable, and the biopharmaceutical industry is hardly the first to face entrenched legacy equipment and processes.

As an example, she cites Kodak, which invented the first digital camera in 1975 but didn’t commercialize it. Aside from its initial technical immaturity, digital photography “would challenge the paradigm of film and chemicals Kodak sold,” Stipa points out. Yet, today, more than 90% of all photos are digital, and film photography is a relatively small niche. Clearly, she says, “It is possible to shift a legacy mindset.

“Our challenge is to find forward-thinking leaders who believe the same way [we do],” Stipa continues. The first two customers have signed on—one engaged in preclinical studies around joint disease, and one focused on animal health—which suggests such leaders are there and are open to new ways of doing things.

“The industry is at a crossroads,” Stipa says. “I see this as an opportunity to help our partners transition from ‘how we’ve always done it’ to a model of bio-agility.”

Phylloceuticals

Location: 800 N. King Street, Suite 304, Wilmington, DE 19801

Focus: Phylloceuticals has developed a plant-based expression system using Lemna (duckweed) as the bioreactor that has produced a mAb in 16 weeks, start to finish. As a multicell eukaryote, Lemna has the cellular machinery necessary to correctly fold and stabilize large, bioactive human molecules.

Some of the forces that shape biopharma cluster development are constants year after year, such as the emergence of startups from university and research institute labs to develop new treatments, thanks to ideas backed by the brains of researchers and executives, and the bucks of serial entrepreneurs and other investors.

But in recent years, several additional unique circumstances have come to reshape how much and especially where biopharmas choose to grow, Matthew Gardner, CBRE Americas Life Sciences Leader, shared with GEN recently.

One is increased acquisition of lab and manufacturing properties by “mid-cap” biopharmas ranging between $2 billion and $10 billion in market capitalization (share price times the number of outstanding shares), as they seek to better control their supply chains by maintaining their own infrastructure in evolving from research- to commercialization-focused drug developers.

“They might have been more likely to lease in a different circumstance. They’ve definitely caught an opportunity to jump in and take ownership. That has been an ongoing trend, and that has been true coast-to-coast in most of the major centers,” Gardner said.

Among investor-owners, Gardner said, another transition has begun from pure-play biopharma real estate landlords to investors with broader portfolios encompassing healthcare—a reflection of how the two fields are increasingly converging. During December 2025 and January 2026, for example, the public real estate investment trust (REIT) Healthpeak shelled out $600 million to close on the acquisition of a 1.4-million square foot, 29-acre campus on Gateway Boulevard in South San Francisco, CA, from the nation’s largest biopharma REIT, Alexandria Real Estate Equities and BXP (formerly Boston Properties).

Those and other investors aim to cash in on the improving climate for biopharmas seeking to raise capital, from a recovering venture capital market to increased merger-and-acquisition (M&A) activity, and, in recent weeks, a revived market for initial public offerings (IPO).

Another key factor in recent cluster-building cited by Gardner is the “reshoring” of manufacturing in the U.S. by global biopharma giants, whether to satisfy growing demand for treatments—especially obesity drugs—or avoid tariffs, or both. While many of those new facilities are in manufacturing-heavy clusters like North Carolina and Greater Philadelphia, others have spread into Maryland and Virginia (the BioHealth Capital Region), and several new biomanufacturing sites have been built or are under construction in emerging clusters outside the Top 10—a trend GEN plans to explore in the coming weeks.

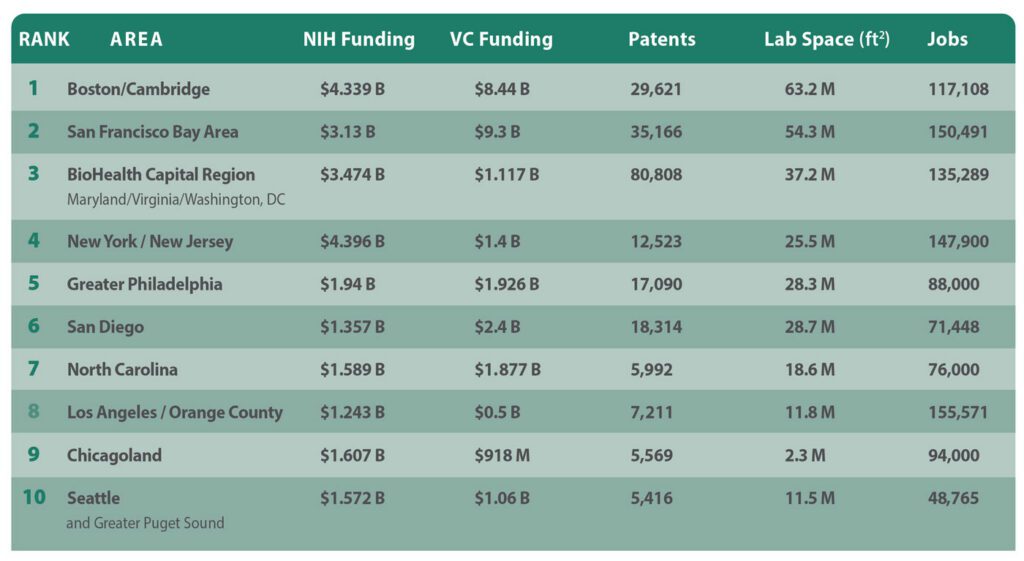

Speaking of top 10 clusters, GEN presents its latest edition of its nationally- and regionally-cited annual A-List of its top 10 U.S. biopharma cluster rankings, designed to show which regions are most competitive in attracting life sciences leaders, companies, and institutions. Over more than a decade, GEN has based its rankings on five criteria:

Patents: Figures from the Patent Public Search database of the U.S. Patent and Trademark Office, showing the number of patent families containing the word “biotechnology” and towns and cities within a given region or state.

NIH funding: Figures for NIH funding were taken from the publicly available NIH Research Portfolio Online Reporting Tools (RePORT) database for the current federal fiscal year through May 4, plus all of fiscal year 2025 (October 1, 2024, through September 30, 2025).

Venture capital funding: Figures for all of 2025 and the first quarter of 2026 as compiled by regional life sciences groups and PitchBook, which joins with the National Venture Capital Association to publish the quarterly Venture Monitor reports.

Laboratory space: The total-size-of-market figure, in millions of square feet, as furnished by regional life sciences groups. In regions that did not compile such information, the figure cited is the highest by any of several commercial real estate companies, including CBRE Group, Colliers, Cushman & Wakefield, JLL, and Newmark.

Number of jobs: The preferred sources for job figures were regional life sciences groups. Alternative sources included commercial real estate firms.

1. Boston/Cambridge, MA

Genentech has agreed to more than triple its space, growing from 30,000 to 100,000 square feet, within 1 Milestone Street at the Harvard University-owned, Tishman Speyer-developed Enterprise Research Campus in Boston’s Allston section [Breakthrough Properties, Studio Gang & Henning Larsen]

Years of growing into the nation’s top biopharma cluster have taken a toll on Boston and adjacent Cambridge, MA: The Wall Street Journal in December highlighted the inability of Boston-area PhDs to find work, while the region faces a glut of life sciences space as biopharmas and real estate developers scale back earlier plans—a 32.7% availability rate according to CBRE, up 70 basis points from Q1 2025. Takeda Pharmaceutical in March eliminated 247 jobs in Massachusetts, where the company has facilities in Lexington, MA, and Cambridge, part of a $1.3 billion restructuring that cut 634 jobs nationwide. Replimune in April chopped 223 jobs at its Woburn, MA, HQ, and Framingham, MA, manufacturing site after the FDA rejected its BLA seeking approval for RP1 [plus Bristol Myers Squibb’s Opdivo® (nivolumab)] for advanced melanoma. In February, Takeda placed 449,140 square feet within three Cambridge buildings on the sublease market, a week after Alexandria Real Estate Equities scrapped plans to convert 401 Park Drive in Boston’s Fenway section into lab space, with CEO and chief investment officer Peter M. Moglia saying the real estate investment trust was pivoting to meet growing demand for office space.

Among the region’s growing life-science companies: Genentech agreed to more than triple its space, growing from 30,000 to 100,000 square feet within One Milestone Street at the Harvard University-owned, Tishman Speyer-developed Enterprise Research Campus in Boston’s Allston section. Hemab Therapeutics (based in Cambridge and Copenhagen) and Seaport Therapeutics (Boston) both priced IPOs on April 30, raising $301.5 million and $254.88 million, respectively—a day after Avalyn Pharma (Boston) garnered $300 million in its IPO. In March, Terrestrial Bio became the first life-science tenant at Allston Labworks (250 Western Avenue) by leasing 42,000 square feet at the mixed-use building within Boston’s Allston neighborhood, while AI Proteins in January inked a 40,000-square-foot lease at 660 Commonwealth Avenue, within Related Beal’s One Kenmore Square in Boston. Regional companies finding buyers in April include Boston-based Kelonia Therapeutics and Cambridge-based Ajax Therapeutics, both to be acquired by Eli Lilly (for up to $7 billion and up to $2.3 billion, respectively) and Framingham-based KalVista Pharmaceuticals, to be acquired by Italy’s Chiesi Group for about $1.9 billion.

Boston/Cambridge enjoys the nation’s largest portfolio of lab space (63.2 million square feet according to industry group MassBio), but was bested by the San Francisco Bay Area in NIH funding (7,037 awards totaling $4.339 billion) following a year of government funding cuts. The region also placed second in VC ($6.85 billion in 2025, says MassBio; $1.59 billion in Q1 2026, according to PitchBook data cited by MassBio), but landed third in patents (29,621 families) and just fifth in jobs (117,108, according to MassBio).

2. San Francisco Bay Area

Eli Lilly Chair and CEO David A. Ricks and Nvidia Founder, president, and CEO Jensen Huang announce the companies’ five-year, $1 billion partnership to create a “Co-Innovation AI Lab” designed to address key challenges in AI drug discovery, announced on January 12 during the J.P. Morgan 44th Annual Healthcare Conference in San Francisco. The lab will be located within the Bay Area. [Nvidia]

Santa Clara, CA-based Nvidia and Eli Lilly electrified the annual J.P. Morgan Healthcare Conference, held in downtown San Francisco each January, by announcing a five-year, $1-billion collaboration to create a “Co-Innovation AI Lab” in the region to address key challenges in artificial intelligence (AI) drug discovery, powered by a supercomputer that went live in February. That welcome news aside, more than one-third of the region’s life-science space is available for lease (33.7% as of Q1, according to CBRE). And more space has entered the market: Pfizer confirmed plans in April to shut down its 164,000-square-foot research facility at 181 Oyster Point Blvd. in South San Francisco, CA, shifting employees to remote jobs. Cushman & Wakefield is marketing the space for sublease. Also, on the market in “South City” is a 21,552-square-foot lab building and surrounding 3.65 acres previously occupied by the U.S. Department of Agriculture, which is selling the building for just under $48 million. In May, Foster City, CA-based Gilead Sciences disclosed plans to lay off 108 employees based in Redwood City, CA, (and 84 in Rockville, MD) following its $7.8-billion acquisition of Arcellx.

Not all the recent news is bad: Gladstone Institutes plans early next year to open approximately 20 new labs employing about 300 scientists within the 105,000 square feet it agreed to lease in March at 1450 Owens Street, within Alexandria Real Estate Equities’ Alexandria Center® for Science and Technology–Mission Bay Megacampus. Natera inked a 62,969-square-foot lease at Brittan West in San Carlos, CA, in February. And last fall, Elon Musk’s Neuralink leased the entire approximately 144,000-square-foot 499 Forbes Boulevard in South San Francisco. On the financing side, SF-based Breakout Ventures in March closed its $114-million Fund III, which aims to invest in founder-led companies applying AI in biopharma, while Palo Alto, CA-based Surf Bio, whose lead investor for its only institutional round was Breakout, was acquired by San Diego-based Halozyme Therapeutics for up to $400 million, in a deal announced in January.

San Francisco and its suburbs topped Boston/Cambridge in VC ($7.8 billion in 2025, $1.5 billion in Q1 2026, both according to PitchBook). The Bay Area is second in three criteria: patents (35,166 families), lab space (54.3 million square feet according to Colliers), and jobs (150,491 according to BIOCOM California, but “more than 147,000” according to CBRE, both from last year). In NIH funding, the region is fourth (5,180 awards totaling $3.13 billion).

3. BioHealth Capital Region (Maryland, Virginia, and Washington, D.C.)

AstraZeneca has expanded the scope of its new manufacturing facility in Rivanna Futures, near Charlottesville, VA, into a $4.5 billion project designed to support manufacturing for weight management, metabolic, and cancer technologies, including antibody-drug conjugates. The project is expected to create 600 permanent jobs. [AstraZeneca]

The BHCR takes in Virginia and Maryland, both of which benefited over the past year from the domestic “reshoring” of biomanufacturing by pharma giants. AstraZeneca in November announced $2 billion in plans for Maryland that include a major expansion of its biologics manufacturing facility in Frederick, MD, and a new clinical manufacturing facility in Gaithersburg, MD. A month earlier, AstraZeneca expanded the scope of its new manufacturing facility in Rivanna Futures, near Charlottesville, VA, into a $4.5-billion project designed to support manufacturing for weight management, metabolic, and cancer technologies, including antibody-drug conjugates. The project is expected to create 600 permanent jobs. Also last fall, Merck & Co. broke ground on a $3 billion, 400,000-square-foot Center of Excellence for Pharmaceutical Manufacturing at its longstanding site in Elkton, VA, while Eli Lilly announced plans for a $5-billion manufacturing facility just west of Richmond, VA, in Goochland County that will be the company’s first-ever dedicated, fully integrated active pharmaceutical ingredient (API) and drug product facility for its bioconjugate platform and monoclonal antibody portfolio. However, a longtime strength of the region—the headquarters presence of the NIH and FDA—is now among its most serious challenges as government funding cuts chopped the workforces of both agencies last year by 3,500 and 1,200 jobs, respectively, though the FDA in recent months has worked to hire 1,000+ new staffers to fill reviewer, inspector, and investigator roles. And in May, Gilead Sciences disclosed plans to lay off 84 employees in Rockville, MD (and 108 in Redwood City, CA) following its $7.8-billion acquisition of Arcellx.

The BioHealth Capital Region fulfills its top-three cluster ambitions by continuing to lead the nation in patents (80,808 families) while placing third in NIH funding (4,665 awards totaling $3.474 billion) and lab space (37.208 million square feet according to JLL data cited by BHCR, including 9.2 million square feet of NIH labs in Bethesda, MD). The region is fourth in jobs (135,298, according to JLL and state data cited by BHCR), but seventh in venture capital ($1.117 billion in 2025, zero in Q1 2026, according to BHCR data).

4. New York/New Jersey

In New Jersey, New Brunswick’s Planning Board in February approved the $468 million H-3, the third phase of the HELIX downtown campus, a 40-story 554,000 square foot tower, for which the city council approved a 30-year PILOT agreement that will generate $1.8 million a year in annual payments in lieu of taxes [DEVCO New Brunswick Development Corp.]

The Big Apple will soon see a big biotech campus emerge, the $1.6 billion, 2-million-plus-square-foot Science Park and Research Campus (SPARC) Kips Bay, projected to create more than 15,000 jobs by combining life-science space with academic and public health facilities. Exterior demolition is scheduled for the third quarter, followed by construction next year. However, Johnson & Johnson has shifted operations of its JLABS@NYC incubator to site owner New York Genome Center, part of a corporate cutback of its incubator network. The 17-member Emerging Technology Advisory Board appointed by New York Gov. Kathy Hochul (D), who is seeking re-election this year, proposed numerous efforts in December to expand life sciences activity statewide, including a $65-million “Excellence” fund and a $40-million pre-commercialization fund. At deadline, the fate of those efforts was unknown despite a tentative agreement on May 7 of a $268-billion state budget.

In New Jersey, New Brunswick’s Planning Board in February approved the $468-million H-3, the third phase of the HELIX downtown campus, a 40-story, 554,000-square-foot tower, for which the city council approved a 30-year PILOT agreement that will generate $1.8 million a year in annual payments in lieu of taxes. In suburban Westchester County, Regeneron Pharmaceuticals is completing a $1.8-billion HQ expansion in Tarrytown but has scuttled earlier plans to expand across the Hudson River into the Rockland County village of Suffern, where the company spent $39 million to buy an old Avon Cosmetics warehouse for conversion into an infectious disease lab and a cold storage facility. In February, Regeneron hired JLL to market the site for sublease.

New York and its northern New Jersey suburbs lead the nation in NIH funding (7,033 awards totaling $4.396 billion) and are third in jobs (147,900, according to Cushman & Wakefield). From there, the region falls to the middle of the pack, placing fifth in VC ($1 billion in 2025 and about $400 million in Q1 2026, both according to PitchBook), and sixth in both lab space (25.5 million square feet, according to Colliers) and patents (12,523 families).

5. Greater Philadelphia

Eli Lilly made history in January by announcing Pennsylvania’s largest-ever biotech project, a $3.5 billion biomanufacturing site planned for Upper Macungie Township, an hour’s drive northwest of Philadelphia. Lilly plans to base 850 jobs at the plant, which will produce retatrutide and other weight loss drugs when it becomes operational in 2031. Lilly also has plans for Philadelphia, namely a 44,000-square-foot Lilly Gateway Labs innovation hub in Center City West at 2300 Market set to open later this year. [Eli Lilly]

Eli Lilly made history in January by announcing Pennsylvania’s largest-ever biotech project, a $3.5-billion biomanufacturing site planned for Upper Macungie Township, an hour’s drive northwest of Philadelphia. Lilly plans to base 850 jobs at the plant, which will produce retatrutide and other weight loss drugs when it becomes operational in 2031. Lilly also has plans for the City of Brotherly Love, namely a 44,000-square-foot Lilly Gateway Labs innovation hub in Center City West at 2300 Market set to open later this year. And, in Philadelphia’s Old City, Thermo Fisher Scientific last November opened its East Coast Advanced Therapies Collaboration Center (ATxCC) within the BioLabs for Advanced Therapeutics incubator.

Thermo Fisher Scientific executives last November celebrated the opening of the biotech tools giant’s East Coast Advanced Therapies Collaboration Center (ATxCC) in Philadelphia’s Old City, within the BioLabs for Advanced Therapeutics incubator. [Thermo Fisher Scientific]

The region’s rich biotech history includes the first gene therapy Luxturna® marketed by Roche-owned Spark Therapeutics—which is completing its $575 million Gene Therapy Innovation Center in University City despite laying off more than half of its Philly staff last year. In March, TerraPower Isotopes announced plans for a $450-million radioisotope manufacturing facility designed to produce actinium-225 for cancer treatments. The project will employ 225, receive $10 million in state grants, and rise within The Bellwether District, the 1,300-acre former Philadelphia Energy Solutions refinery site. Greater Philadelphia has long benefited from innovations from its institutions, two of which won more than $100 million in NIH funding during the 2025 federal fiscal year, the Perelman School of Medicine at the University of Pennsylvania to Children’s Hospital of Philadelphia (CHOP)—which last year treated KJ Muldoon (“Baby KJ”), the world’s first patient to receive a personalized CRISPR gene-editing therapy (for CPS1 deficiency). The region’s needs for more C-suite talent and venture capital remain persistent challenges to cluster growth, stakeholders told The Philadelphia Inquirer in December, though Audrey Greenberg, chair of corporate development and “Mayo Venture Partner” at Mayo Clinic and founder of AG Capital Advisors, told the Inquirer: “I’m going to be starting my companies all here in Philadelphia, because that’s where I am.”

Greater Philadelphia improved the most this year, climbing two positions in this year’s A-List after remaining fifth in patents (17,090 families) and rising to fifth in lab space (25.9 million square feet, according to Colliers’ data cited by Pennsylvania’s Department of Economic Development or DECD) and NIH funding (3,201 awards totaling $1.94 billion). The region jumped four spots to fifth in VC ($1.31 billion in 2025, $616 million in Q1 2026, says Colliers), but dipped to seventh in jobs (88,000, also according to DECD), including nearly 10,000 with cell and gene therapy expertise.

6. San Diego

Novartis broke ground in February on a $1.1 billion, 466,000-square-foot global Biomedical Research center in San Diego, expected to house 1,000 employees when operational in 2029, three months after opening a radioligand therapy manufacturing facility for cancer treatments in Carlsbad, CA. [Novartis]

The Biotechnology Innovation Organization (BIO) expects to draw 20,000 to its BIO International Convention when it returns this month to the San Diego Convention Center. The region remains a vibrant life-sciences cluster: Novartis broke ground in February on a $1.1-billion, 466,000-square-foot global Biomedical Research center in San Diego, expected to house 1,000 employees when operational in 2029, three months after opening a radioligand therapy manufacturing facility for cancer treatments in Carlsbad, CA. Eli Lilly in March completed its $1.2-billion acquisition of home-grown Ventyx Biosciences—months after the pharma opened a Lilly Gateway Labs innovation hub with Alexandria Real Estate Equities in Torrey Pines. The J. Craig Venter Institute—whose founder died April 29 at age 79—plans this summer to move its West Coast headquarters from the University of California San Diego campus in La Jolla to the downtown Research and Development District (RaDD), a $1.6-billion, 1.7-million-square-foot campus on the city’s Pacific coastline completed last year by San Diego-based developer IQHQ—which is fighting an investor’s fraud allegations related to a $50-million investment in 2020. Home-grown F5 Therapeutics (up to 10 employees) folded in March, while two other San Diego biotechs laid off employees this year: Gossamer Bio (65 employees, nearly half its workforce, as of May 15, following a Phase III trial failure) and BioAlta (70% of its staff, which was 41 as of December 31, 2025). In February, San Diego drug developer Iambic Therapeutics inked an up-to-$1.7-billion collaboration with Takeda Pharmaceutical, which will use Iambic’s AI technologies and wet lab capabilities to design and develop small molecule drugs. And global contract development and manufacturing organization (CDMO) Bora Biologics, in January, opened a $30-million expanded manufacturing facility with two to four 2,000-liter bioreactors, corresponding seed trains, and advanced downstream processing equipment.

“America’s Finest City” and vicinity stayed third in VC ($1.9 billion in 2025, says PitchBook, $743 million in Q1 2026 according to a GEN spot-check of recent deals) and fourth in patents (18,314 families) but dipped to fifth in lab space (28.685 million square feet, according to CBRE). While the San Diego region last year rose to ninth in NIH funding (2,001 awards totaling $1.357 billion), it slid to ninth in jobs (71,448, according to year-old BIOCOM California data).

7. North Carolina

Roche’s Genentech subsidiary in January expanded to $2 billion its planned investment in its first East Coast manufacturing facility in Holly Springs, NC, which broke ground last year and is set to support 500+ manufacturing jobs when operational by 2029. [Genentech]

Always strong on drug manufacturing, North Carolina is among the biggest beneficiaries of biopharma’s reshoring push. In April, AbbVie announced a $1.4-billion, 185-acre drug production facility in Durham County near Research Triangle Park (RTP), expected to employ 734. Roche’s Genentech subsidiary in January expanded to $2 billion its planned investment in its first East Coast manufacturing facility in Holly Springs, NC, which broke ground last year and is set to support 500+ manufacturing jobs when operational by 2029. And in November 2025, Novartis said it will expand Tar Heel State operations into a flagship manufacturing hub by adding capabilities for sterile filling of biologics into syringes and vials at its current Durham site, constructing two new Durham facilities for manufacturing biologics and sterile packaging, and building a new Morrisville, NC, site to produce solid dosage tablets and capsules, including packaging. Morrisville is where Novartis also plans to build a 56,200-square-foot facility focused on API manufacturing for solid dosage tablets, capsules, and RNA therapeutics, a project announced April 30. Manufacturing sites account for most of the combined $24.5 billion in new or expanded facilities with a potential 15,000+ new jobs that life sciences companies have announced statewide since 2021, according to the state-funded North Carolina Biotechnology Center. As for startups, Raleigh-based Slate Medicines launched in February with $130 million in Series A financing to fund development of therapies led by its migraine candidate, the anti-PACAP monoclonal antibody SLTE-1009 licensed from Zhongshan, China-based DartsBio Pharmaceuticals, and set to start Phase I trials in mid-2026.

The Tar Heel State climbed to fourth in VC ($1.6 billion in 2025, $276.8 million in Q1 2026, both according to the state-funded North Carolina Biotechnology Center). But North Carolina showed consistency on the other criteria, ranking seventh in NIH funding (2,248 awards totaling $1.589 billion) and lab space (18.6 million square feet, according to JLL), and eighth in jobs (76,000, says the Center) and patents (5,992 families).

8. Los Angeles / Orange County, CA

Amgen executives mark the groundbreaking for the biotech giant’s $600 million center for science and innovation being built within its Thousand Oaks, CA, headquarters campus, set to integrate Research & Development and Process Development teams to smoothen the transition from drug discovery to commercial manufacturing. [Amgen]

The region’s biopharma anchor Amgen broke ground last fall on a $600-million center for science and innovation being built within its Thousand Oaks, CA, headquarters campus, set to integrate research & development and process development teams to smooth the transition from drug discovery to commercial manufacturing. “With the first shovel in the ground, we’re reaffirming something essential: We discover here, we manufacture here, we deliver for patients from Thousand Oaks to all around the world,” Amgen chairman and CEO Robert A. Bradway said. Regional industry group BioscienceLA CEO Stephanie Hsieh recently acknowledged the region’s fragmentation as a challenge—from 88 cities in LA County alone, to the numerous county, city, and private agencies focused on growing the bioindustry— while citing strengths such as corporate anchors Amgen, Takeda Pharmaceutical, and Gilead Sciences-owned Kite Pharma, plus institutions like USC, UCLA, Cedars-Sinai, and City of Hope.

California signaled interest in growing the region’s biopharma industry last August when the state-funded California Jobs First Regional Investment Initiative awarded $23.92 million to a coalition led by Los Angeles County’s Department of Economic Opportunity (DEO) toward four programs intended to create 10,000 jobs by 2030. Most of the money ($19 million) was approved for a DEO revolving loan fund to support startups, especially those looking to graduate from the Larta Institute’s commercialization and capital access accelerator into lab space within Los Angeles County. Larta was awarded $3.3 million to expand its Heal.LA Bioscience & Healthcare Accelerator and assist small startups via its Larta Impact Fund, a revolving loan fund.

Los Angeles/ Orange County would still lead the nation in jobs, based on a year-old BIOCOM California tally of 155,571, which also includes San Bernardino and Ventura counties; figures run as low as 116,000, compiled last year for the four counties plus Riverside and Santa Barbara counties (regional industry group SoCalBio). The region finished seventh in patents (7,211 families), eighth in lab space (11.7 million square feet, according to JLL), and 10th in both NIH funding (1,911 awards totaling $1.243 billion) and VC ($500 million in 2025, zero in Q1 2026, according to PitchBook).

9. Chicagoland

AbbVie plans to build two new active pharmaceutical ingredient (API) manufacturing facilities totaling $380 million at its campus in North Chicago, IL, where the biopharma giant is headquartered. [AbbVie]

At least one developer has pivoted to a large non-biotech tenant to help fill a Chicago campus once envisioned as a life-sciences mecca: Trammell Crow in March inked a $100-million, 169,860-square-foot lease with candy/chocolate giant Mars to base 600 jobs at 400 North Aberdeen Street within the Fulton Market campus. Other biotech spaces are in the works: In North Chicago, Rosalind Franklin University of Medicine and Science plans to nearly double the size of its Helix 51 biomedical incubator to just under 13,000 square feet by adding 6,000 square feet of new lab and office space, citing growing demand from early-stage biotechs. The expansion is expected to create space for up to 10 additional companies. Also in North Chicago, home-grown AbbVie announced plans to build two new API manufacturing facilities totaling $380 million at its campus in the Chicago suburb. The facilities—designed to support production of next-generation neuroscience and obesity treatments—are set to be fully operational in 2029. However, AbbVie opted to build its planned $1.4-billion biomanufacturing campus not in North Chicago but 821 miles southeast in Durham, NC. Across Illinois, biotech stakeholders have applauded Gov. J.B. Pritzker (D) for proposing to sweeten the state’s Research & Development Tax Credit program by allowing companies to transfer their credits for cash. “This is a transformative step for our startup and growth-stage ecosystem,” stated John Conrad, president and CEO of the Illinois Biotechnology Innovation Organization (iBIO). Pritzker is seeking a third term in November vs. Darren Bailey (R).

The Windy City and vicinity rank sixth in both NIH funding (2,658 awards totaling $1.607 billion) and jobs (94,000, according to statewide industry group Illinois Biotechnology Innovation Organization or iBIO). The region places ninth in patents (5,569 families) and VC ($917.677 million in 2025, says iBIO, zero in Q1 2026,

10. Seattle

AGC Biologics, a global CDMO, expanded its regional research footprint last fall by signing a 37,575-square-foot lease at Element Research Center in Bothell, WA. [AGC Biologics]

Seattle and the Greater Puget Sound’s strong base of academic and other nonprofit research institutions helped the region achieve consecutive years of Nobel laureates: Mary E. Brunkow, PhD, of the Institute for Systems Biology in Seattle co-won the 2025 prize in Physiology or Medicine a year after David Baker, PhD, director of the Institute for Protein Design at University of Washington (UW), co-won the 2024 prize in Chemistry. A UW spinout, Seattle-based 3D tissue model developer Curi Bio, closed in December on a $10-million Series B financing led by South Korean contract research organization DreamCIS. In April, Achieve Life Sciences (based in Seattle and Vancouver, BC) announced an up-to-$354 million private placement whose purposes include funding a Phase III trial and future commercialization of e-cigarette cessation candidate cytisinicline, while Athira Pharma landed up to $236 million in conjunction with acquiring exclusive rights from Sermonix Pharmaceuticals to the Phase III metastatic breast cancer candidate lasofoxifene. AGC Biologics, a global CDMO, expanded its regional research footprint last fall by signing a 37,575-square-foot lease at Element Research Center in Bothell, WA. However, Astellas Pharma told Washington state officials in April it will shutter the Seattle site of its Universal Cells subsidiary by 2028, with 50 employees to be impacted via layoffs or transfers to South San Francisco, CA, or Westborough, MA.

Seattle and its suburbs placed highest at eighth in both NIH funding (eighth with 1,892 awards totaling $1.572 billion) and VC ($1.06 billion in 2025, zero in Q1 2026, according to industry group Life Science Washington). The region was ninth in lab space (11.46 million square feet, according to regional real estate firm Flinn Ferguson Cresa) and 10th in both jobs (48,765 according to Life Science Washington) and patents (5,416 families).

Erik Terjesen Managing Director Silicon Foundry, a Kearney Company

Clinical development has become the most resource-intensive stage of drug innovation. Across the industry, clinical trials consume 60–70% of total R&D spending, a proportion that continues to rise as trials grow more complex, more data-heavy, and more operationally demanding. The irony is that while science has advanced dramatically, the underlying model for running trials still reflects assumptions from a pre-digital era. The result is an ecosystem in which timelines stretch, costs multiply, and meaningful efficiency gains remain elusive.

AI has reached a level of maturity capable of reshaping this landscape, but its potential remains constrained by a fundamental issue the industry has been slow to confront. The data used to power these systems was never designed with AI in mind. In fact, the true crisis in clinical development today is structural and deeply rooted in how trial data is organized, contextualized, and interpreted.

Why trial models are failing

Clinical trials were built for physical sites, paper workflows, and slow-moving systems. Modern trials look nothing like that. They are distributed, data-heavy, biomarker-driven, and increasingly adaptive, yet they still run on infrastructure designed for a simpler era.

For years, clinical operations have been organized around sites and checklists rather than continuous insight. Data moves in bursts, workflows remain fragmented, and systems rarely talk to one another. Precision medicine expanded what trials could ask of data, but the way trials actually operate has barely evolved.

The problem isn’t only speed or scale. It’s also the quiet erosion of efficiency in places trial plans rarely account for. Across the industry, leaders describe a growing layer of “invisible waste”: repeated handoffs, duplicative manual work, incompatible data structures, and everyday operational friction that steadily stretches timelines and drives up costs, even though it seldom appears in formal project plans.

AI changes the equation, but only if trial data can support it.

Why AI stumbles in pharma

There is no shortage of AI talent, tools, or ambition in the life sciences sector. What is scarce is data that AI can meaningfully learn from. Most early AI-for-clinical-trials initiatives failed not because the models were immature, but because the data they were fed was not curated with clinical intent.

Models trained on large public corpora can identify patterns, but they lack clinical judgment. If the data is unstructured, inconsistently labeled, or lacks contextual metadata, the model will draw the wrong conclusions with absolute confidence. The well-known “ruler problem”—in which an AI system learned to detect malignant skin lesions based on the presence of a ruler beside the lesion—illustrates how easily models latch onto irrelevant signals.

2. Pharma’s internal data is both rich and unusable.

Organizations hold decades of trial data, but these assets are rarely AI-ready. Different study teams, CROs, and geographies used different standards. Biomarker and imaging data are often stored in systems that cannot communicate with EDC or safety platforms. And clinical notes, PDFs, and unstructured documents require interpretation that models cannot perform without curated training sets.

AI amplifies the quality of the data it is given. If the input is clinically inconsistent, overgeneralized, or disconnected from the trial context, the outputs will be clinically meaningless.

Recognizing this, many pharmas are now investing heavily in curated internal datasets, governance frameworks, and senior AI leadership, often in the form of newly created chief AI officer roles. These leaders are tasked with not just deploying tools, but rebuilding the data infrastructure from which future AI insights will emerge.

The new AI toolkit for clinical trials

Once the data foundation is strong, AI becomes a force multiplier across the entire trial lifecycle. Several categories show particularly high near-term impact potential.

Clinical-grade language models: Purpose-built models that ingest curated internal datasets can help draft protocols, refine eligibility criteria, flag operational risks, and interpret historical trial performance. Unlike general-purpose systems, these models are tuned to reason the way experienced clinical scientists do.

Multimodal AI for patient stratification and endpoint optimization: Integrating imaging, labs, digital biomarkers, and historical trial outcomes enables more precise cohort selection and improves the likelihood of detecting true therapeutic effect. These tools help convert today’s complex data streams into actionable insights.

Synthetic and hybrid control arms: While still emerging, these approaches reduce dependence on large traditional control cohorts by incorporating real-world evidence and model-generated comparators when appropriate. The result is faster recruitment and more efficient statistical design.

AI agents for operations: Operational agents can triage site queries, assist with eligibility adjudication, coordinate scheduling, and draft routine documentation. They are particularly helpful in reducing the administrative burden that slows trial execution.

The most underestimated category, and the one with the most long-term potential, is clinical-driven AI, where the model is trained to interpret clinical data the way a researcher with a PhD or a clinician would. This approach addresses the core issue of context, which is essential for decision-making in regulated environments.

From site-centric to data-centric trials

Trials are gradually evolving away from rigid site-based infrastructure and toward data-centric execution. AI accelerates this shift by enabling continuous monitoring, adaptive decision-making, and greater representation across diverse populations. The next phase of this transition requires progress in several areas:

Reliable digital biomarkers collected via wearables and sensors that feed directly into the trial data ecosystem.

Real-world evidence integration that allows trial designs to incorporate external data while maintaining regulatory rigor.

Improved cohort diversity, supported by AI-driven recruitment models that identify and engage underrepresented populations.

Always-on trial oversight, where adaptive protocols adjust based on real-time data rather than periodic interim reviews.

As these elements mature, trials will resemble dynamic learning systems rather than static sequences of predefined events.

Pharma cannot do this alone

The clinical-trial innovation ecosystem is now incredibly fragmented. A myriad of startups, many founded within the last five years, are attempting to solve different slices of the trial process. Some focus on recruitment; others on protocol simulation, operational automation, predictive enrollment, or digital biomarker analysis.

This fragmentation creates noise but also opportunity. The organizations that succeed will be those that adopt a hybrid strategy, in which internal data expertise is paired with carefully selected external partners. Evaluating early-stage companies requires disciplined technical assessment and an understanding of which partners can meet enterprise requirements in a regulated environment.

Pharma organizations also face a structural talent challenge. The best AI engineers often gravitate toward startups rather than large enterprises. This dynamic reinforces the need for partnership models that combine internal governance with external innovation rather than relying exclusively on one or the other.

What AI can (and cannot) fix

While AI can dramatically shorten timelines and improve decision-making, it is not a cure-all. It will not rescue a flawed trial design, replace human oversight, or eliminate the need for regulatory rigor. What it can do is accelerate the work around those elements, optimizing how protocols are developed, how patients are selected, how data is interpreted, and how milestones are achieved. The organizations that reap the greatest benefit will be those with disciplined data stewardship and a willingness to rethink long-held operational assumptions.

Erik Terjesen is the managing director at Silicon Foundry, a Kearney Company

Like any complex system, the cell depends on a tightly regulated quality control network to maintain order and prevent the accumulation of harmful proteins. This network governs protein homeostasis, including the synthesis, folding, trafficking, and ultimately the clearance of proteins. When these processes fail, aberrant or misfolded proteins can accumulate and drive disease.

Targeted protein degradation (TPD) therapeutics seek to harness this intrinsic quality control machinery to selectively eliminate disease-causing proteins. Central to this approach is the principle of induced proximity, in which a designed molecule brings a target protein into close contact with a cellular effector, triggering its removal through endogenous degradation pathways.

Two major systems underpin these processes. The ubiquitin-proteasome system governs the degradation of intracellular, soluble proteins, where targets are tagged with ubiquitin by a cascade of enzymes, including E3 ubiquitin ligases, and directed to the proteasome for destruction. In parallel, lysosome-mediated pathways handle larger, membrane-bound, extracellular, or aggregated proteins by routing them through endocytic or autophagic mechanisms for degradation.

Building on these natural systems, a growing toolkit of TPD modalities has emerged. For example, proteolysis-targeting chimeras (PROTACs) exploit the ubiquitin-proteasome system, while newer approaches such as lysosome-targeting chimeras, including sortilin-based lysosome targeting chimeras (SORTACs), extend degradation to extracellular and membrane-associated proteins. Molecular glues, by contrast, stabilize interactions between E3 ligases and target proteins without requiring a bifunctional design, further expanding the scope of induced proximity strategies. Additional degrader technologies are being developed.

Although first described more than 25 years ago, TPD is now entering a phase of rapid maturation and increasing therapeutic relevance. By operating through catalytic, event-driven mechanisms rather than traditional occupancy-based inhibition, these approaches offer the potential to address previously “undruggable” targets, overcome resistance mechanisms, and deliver more durable clinical responses. At the same time, key challenges remain, including expanding access to extracellular targets, improving target validation strategies, and navigating an increasingly complex and data-rich development landscape.

Tackling the extracellular frontier

Early TPD efforts have primarily targeted cytosolic proteins, leaving extracellular and membrane-bound targets (estimated to comprise about 40% of the human proteome) largely unaddressed.

“Many key drivers of disease, including inflammatory cytokines, protein aggregates, and secreted factors, remain inaccessible to conventional PROTAC-based approaches,” says Simon Glerup, PhD, co-founder and CSO, Draupnir Bio, a spinout from Aarhus University (Denmark).

Simon Glerup, PhD, co-founder and CSO, Draupnir Bio and Lab: Lab photo from left: Jonas Lende, Casper Larsen, Simon Glerup, Marianne Kristensen, Camilla Gustafsen, Amanda Simonsen, Line Slemming.

The company is addressing this gap by utilizing its proprietary SORTAC platform, a modular, small-molecule technology designed to degrade extracellular proteins by harnessing the natural lysosomal clearance pathway. Glerup notes that “these targets are central to diseases such as neurodegeneration and inflammation, yet remain difficult to drug with existing modalities.”

SORTACs are bifunctional small molecules composed of a sortilin-binding module linked to a target-binding ligand, enabling formation of a ternary complex between an extracellular disease protein and the lysosomal receptor sortilin, which drives internalization and degradation in lysosomes. Glerup elaborates, “Unlike antibody-based or intracellular TPD approaches, SORTACs combine the advantages of small molecules (such as potential oral delivery and tissue penetration) with catalytic, event-driven pharmacology. The platform has demonstrated hallmark TPD properties, including ternary complex formation and catalytic turnover, with in vitro and in vivo degradation of therapeutically relevant targets.”

Glerup emphasizes that SORTACs enable degradation of both soluble and membrane-associated proteins and leverage receptor recycling to drive sustained target clearance.

The company has launched a multi-partner Danish initiative, DESYNA (Degradation of Extracellular α-SYNuclein Aggregates) in collaboration with Aarhus University, focusing on Parkinson’s disease. Accumulation of α-synuclein aggregates is a key driver of disease, and the approach aims to selectively degrade these pathogenic species and halt their progression.

Glerup believes extracellular TPD represents the next major wave of innovation in the field. “By extending TPD beyond the cell’s interior, the cytosol, SORTAC has the potential to unlock a large and previously inaccessible target space. With growing validation and collaborative efforts such as DESYNA, there is strong reason for optimism that this approach can deliver transformative therapies for diseases that currently lack effective treatment options.”

Enabling TPD workflows

Advancing TPD depends on a coordinated ecosystem of tools that support target validation, mechanistic interrogation, and translational predictions. Within this context, attention is increasingly focused on the central challenge of translating mechanistic promise into consistent patient benefits.

Hannah Maple, PhD Senior Director Bio-Techne

“I think we are on the brink of seeing TPD and induced proximity truly usher in a new era in drug discovery as we await the first clinical approval of a PROTAC degrader,” says Hannah Maple, PhD, senior director at Bio-Techne®. At the same time, she notes that “one of the challenges with this as a new drug modality is to gain a deeper understanding of where the maximum patient benefit lies from a target and indication perspective.”

That uncertainty places renewed emphasis on target validation strategies. Maple elaborates, “Driving efficacy versus standard of care in a predictable way remains a challenge, despite in many cases strong mechanistic rationale for degradation versus inhibition of a particular target. For this reason, I would keep target validation high on the list of key challenges for the field as it relates to driving clinical impact and patient benefit with this technology.”

To support this critical transition, Maple says Bio-Techne has established long-standing collaborations with leading research groups to co-develop new technologies and support training of the next generation of TPD scientists. The company has also built an integrated portfolio of tools spanning biological reagents, chemical probes, and assay platforms with TPD-focused capabilities across its R&D Systems portfolio brand, including the Tocris small-molecule products.

Maple provides an example. “Some of the most useful categories of tools for target exploration and validation in the context of TPD are the R&D Systems’ Tocris Tag Degradation Platforms and self-labeling protein tag platforms.” These approaches involve fusing a small protein tag to the protein of interest and pairing it with a complementary small-molecule ligand that binds the tag. The tag ligand is typically bifunctional and can be developed to recruit an E3 ligase to the protein-of-interest, eliciting degradation in a controllable, tunable manner.

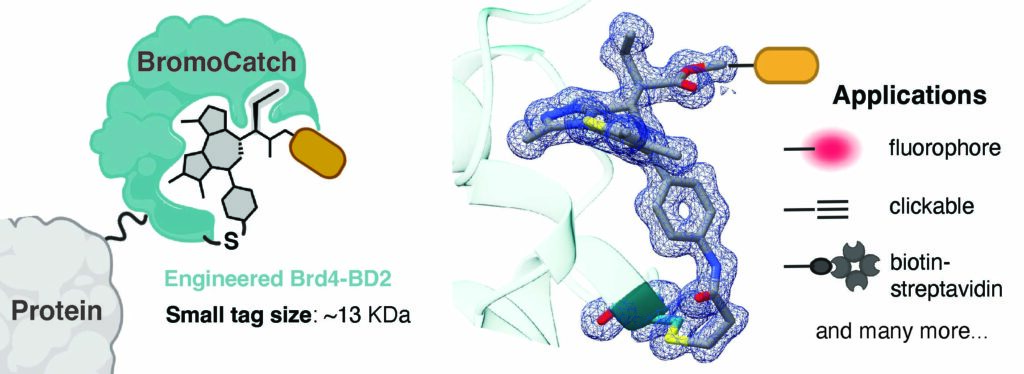

Within this ecosystem, protein-level tools support target interrogation and validation. Maple highlights self-labeling tag systems as particularly valuable. “Through our R&D Systems brand, we have built a leading portfolio of these technologies, and very recently launched BromoCatch, a next-generation self-labeling tag platform that was co-developed with [the lab of Alessio Ciulli, PhD] at the Centre for Targeted Protein Degradation, University of Dundee. BromoCatch represents a powerful, modular platform that uses a low molecular weight protein tag. The benefit of this approach is to minimally perturb the native localization or function of the protein being tagged, versus prior larger tags that could cause undesired functional effects.”

BromoCatch is a small, rationally designed self-labeling tag platform for targeted protein analysis, manipulation, and degradation. [Bio-Techne]

Complementing these approaches, the R&D Systems portfolio provides targeted degradation reagents such as dTAG-13, a heterobifunctional degrader used in tag-based systems to selectively eliminate engineered proteins of interest, offering a chemical alternative to genetic knockdown approaches.

Maple reports that another impactful technology of Bio-Techne’s R&D Systems portfolio is their Simple WesternTM automated western blot instruments. She explains, “TPD heavily relies on western blotting, but scaling screening campaigns using this as a primary assay is a huge time and resource drain, with variable data quality and poor reproducibility. Simple Western technology allows researchers to get reliable, reproducible and quantitative degradation data on a fully automated instrument.”

Enhancing pipeline intelligence

Flavio Lima Bianchi Lead Research Analyst Beacon by Hanson Wade

Keeping pace with the fast-moving TPD landscape can be daunting. “Part of the problem is that reliable data is hard to come by, particularly in regards to the advancements coming out of China, with developers still relying on their own, in-house methods to generate viable, orally bioavailable lead candidates at the cost of significant time and investment,” observes Flavio Lima Bianchi, lead research analyst at Beacon by Hanson Wade.

As evidence of this challenge, Bianchi notes that despite PROTACs comprising roughly a third of the overall TPD landscape, “to date less than five percent of PROTACs have managed to progress into the clinic and only a select few drugs have reached late-state, pivotal studies.”

The company is addressing these limitations in several ways. “We aggregate all available TPD data and render it into an easily searchable and digestible format. Too often is information siloed within organizations and, perhaps more importantly, failed degraders are rarely published or are quietly swept under the rug.”

He continues, “Beacon leverages a mixture of publicly available and proprietary data obtained directly from developers to track every single TPD program globally and to lift the lid on both the successes and the failures, enabling developers to make better, more informed decisions.”

While investigators relying on in-house methods may spend significant time searching available information, Bianchi emphasizes that their platform extends well beyond data access. “Beacon TPD is a subscription-based intelligence platform, providing users the ability to search comprehensive, curated preclinical, clinical, and commercial data across the induced proximity landscape. Aside from this primary search and retrieve function, Beacon’s additional functionalities include analyst reports, conference summaries, weekly newsletters and alerts, all designed to keep users abreast of the latest development within their field of interest.”

Broadening TPD horizons

Bio-Techne’s Maple envisions TPD expanding well beyond its original scope. “I think about TPD as one portion of a broader induced proximity revolution. The basic principles and technological breakthroughs that have driven TPD can be applied to targeted protein localization, stabilization, modulation, etc. This opens new optionality from a therapeutic standpoint and is also opening entire new fields of basic research enabled by these new principles and chemical tools.”

In April 2025, the U.S. Food and Drug Administration (FDA) released a strategic roadmap to make animal testing the exception for preclinical safety and toxicity studies within the next three to five years. Central to that vision is the adoption of validated new approach methodologies (NAMs), including organ-on-chip systems. The National Institutes of Health reinforced that shift the same month by requiring that all new notices of funding involving animal models incorporate human-focused approaches such as organ chips and other NAMs. Similar changes are emerging globally. In November 2025, the U.K. government published its roadmap to largely phase out animal testing in research while accelerating the development and validation of alternative methods.

For organ-on-chip developers, growing interest from federal agencies is a welcome trend. They are currently generating the data necessary to show that their technologies can work in stringent regulatory environments. However, there are still outstanding questions around validation standards, regulatory expectations, and how NAM data will be evaluated in submissions. At the same time, adoption remains slow, with drug developers continuing to rely largely on established animal models, which command billions in investment compared to the much smaller organ-chip sector.

Still, it is clear that momentum is building behind NAMs. And in response, organ-chip developers are stepping up to ensure that their platforms can produce results when the time comes.

From space flight to lab scale-up

When the Artemis II astronauts launched their historic 10-day journey around the Moon in April 2026, they carried some unusual cargo: organ chips containing cells from their bone marrow. The chips are part of the AVATAR (A Virtual Astronaut Tissue Analog Response) investigation, which is using organ-on-chip devices to study the effects of deep-space radiation and microgravity on human health.

Emulate’s organ chips played a pivotal role in the recent Artemis II lunar mission. The so-called AVATAR experiment could change how space agencies study the effects of radiation and microgravity impact human health. [Emulate

Before the trip, cells from the astronauts were harvested to create two sets of bone marrow chips: one set traveled beside the crew aboard their spacecraft, while another remained on Earth. The idea was to compare both sets of chips when the astronauts returned to Earth. More broadly, the AVATAR project also aims to provide proof-of-concept for including human organ chips in future missions.

In 2025, Emulate announced that its organ-chip technology was selected to accompany the astronauts on their lunar fly-by. It is an exciting project for Emulate, which commercializes human organ-chip technology developed at the Wyss Institute for Biologically Inspired Engineering at Harvard University. But it is only one of several activities that the company has been involved in the recent past. The company’s liver organ chips were one of the first to be accepted for the FDA’s Innovative Science and Technology Approaches for New Drugs (ISTAND) program, which supports tools that fall outside the scope of existing qualification programs but may still be useful for drug development.

Lorna Ewart, PhD Chief Scientific Officer Emulate

In a conversation with GEN, Lorna Ewart, PhD, Emulate’s chief scientific officer, described 2025 as a pivotal year both externally—with announcements from multiple federal agencies promising increased support for organ chips—and internally, with the launch of Emulate’s new instrument, AVA, in June 2025 to address what Ewart describes as “key operational challenges” with the company’s first-generation platform. AVA has a higher throughput than its predecessor, enabling microfluidic workflows across 96 parallel organ chips or “emulations” in a single run. The company claims that it is the first organ-on-chip workstation to combine high-throughput microfluidic tissue culture with automated imaging in a self-contained environment.

Interest in the instrument to date has come primarily from large pharmaceutical companies and mid-sized biotech firms, who need to run large numbers of chips in parallel. But, Ewart says, there is also strong interest from academic institutions and government agencies. Some of that interest is driven by AVA’s much smaller footprint. Compared to Emulate’s first-generation system, AVA is a compact benchtop system that does not require multiple incubators. The company has also reduced the size of each emulation, or chip equivalent, by about 50%, meaning that the new platform requires fewer cells and uses less media, helping to keep experimental costs down. “Academics are actually quite excited about getting their hands on it and looking at it as a core lab instrument where multiple labs will be able to use it.”

AVA also addresses concerns about reproducibility, a consistent source of worry for drug developers, and one that Emulate has made a priority. The company has shared data showing that its liver-chip biology is reproducible both internally and externally in laboratories using AVA. The company has also taken steps to minimize technical variability within experiments as well as bias when running AVA at scale. “We need to make sure that the first chip array looks the same as chip array eight,” Ewart says. “If it doesn’t, there’s variability across those different [chip arrays] that will impact the way that a user can design, what we would refer to as a fully burdened experiment.”

More complex, automated models

When it first launched, U.K.-based organ-on-chip company CN Bio started with a liver-on-a-chip platform, but has since expanded to include various organ models, including intestine, lung, and kidney. The company’s commercial platform is built on technology developed in the laboratory of Linda Griffith, PhD, at the Massachusetts Institute of Technology.

Tomasz Kostrzewski, PhD Chief Scientific Officer CN Bio

Currently, CN Bio has applications in multiple arenas, including safety, toxicology, and disease modeling. “For example, in the toxicology space, we have a very well-known and well-utilized model of drug-induced liver injury,” Tomasz Kostrzewski, PhD, the company’s CSO, tells GEN. That model is being utilized by several global clinical research organizations to offer assays as a service. The company also has a multi-organ system that links its intestine and liver chip models, which can be used to predict the oral bioavailability of drugs, and a range of disease models for metabolic liver disease, chronic obstructive pulmonary disease, and more.