Background: Self-harm is the strongest risk factor for suicide and an important outcome for mental health care. Although prevalent in clinical populations, it is often imprecisely captured in routinely collected clinical data, where it is often recorded and stored as unstructured free text. Contemporary language models, such as GPT (OpenAI) and Gemini (Google), can analyze free-text clinical notes, but such models may violate data governance of processing sensitive patient data. Objective: This study aimed to evaluate whether a privacy-preserving language model running entirely within an institution’s secure computing infrastructure (here, the UK National Health Service [NHS]) could accurately identify the presence and timing of self-harm using electronic health records from secondary mental health care. Methods: Clinical notes were drawn from Oxford Health NHS Foundation Trust using a multistage workflow: (1) a random sample of 1000 patients with a psychiatric diagnosis, defined according to the (; codes F00–F99); (2) candidate-note identification using a Gemma3-4b language model to flag notes containing self-harm content; and (3) from those candidates, 1352 randomly sampled notes were selected for expert annotation, resulting in gold-standard corpus enriched for self-harm content. Clinical notes were annotated for the presence of self-harm and its timing (≤90 days, >90 days, or unknown). A privacy-preserving locally served 27-billion-parameter Gemma 3 language model (“Gemma3-27b”) was used as the core model. Prompts were systematically developed and refined using a labeled development set to identify self-harm and generate a structured output per clinical record. Gemma3-27b performance was compared against a strong baseline multilabel text classification model based on robustly optimized BERT pretraining approach (RoBERTa), a transformer-based language model architecture. Model performance was evaluated using precision, recall, and the -score (harmonic mean of precision and recall), with 95% CIs estimated from 1000 bootstrap samples with replacement. Results: Gemma3-27b outperformed the RoBERTa classifier across all categories, achieving Precision=0.92, Recall=0.92 (sensitivity), and -score=0.92 for notes containing self-harm, and Precision=0.97, Recall=0.97 (specificity), and -score=0.97 for notes without self-harm. For the 51 notes labeled as recent self-harm in the held-out test set, Gemma3-27b achieved Precision=0.84, Recall=0.75, and -score=0.79. The global weighted -score of Gemma3-27b across all categories was 0.88, compared to 0.85 for RoBERTa. Conclusions: With systematic prompt development on a labeled development set, but no gradient-based fine-tuning, the current Gemma3-27b language model matched or exceeded a fine-tuned RoBERTa classifier for ascertaining self-harm events and their timing. Aggregate gains were modest, while improvements were largest in the most challenging, lower-frequency timing categories. On a simplified binary recent-versus-other task, RoBERTa performed marginally better, indicating that supervised classifiers remain highly effective when the task is simplified and sufficient labeled data exist. This work demonstrates the technical feasibility of privacy-preserving self-harm detection within a secure NHS research environment.

The global health care sector is under increasing strain.

Decades of chronic underinvestment and constraints in recruitment have coincided with a surge in demand for services for aging populations. Gaps in provision are already taking a toll, with fragmented access to care and high rates of stress and burnout among staff. And it’s getting worse. The World Health Organization has warned that current shortfalls will increase to 11 million workers by 2030.

In their urgent hunt for a solution, many health-care providers are now pinning their hopes on agentic AI, with more than two-thirds (68%) having already adopted AI agents into their workforce, according to KPMG.

The technology is being deployed to automate complex back-office processes, collaborate with medical teams, and even triage patients, all in a bid to reduce the cognitive load on clinicians and improve quality of care for patients as the supply of human health-care workers dwindles.

A different type of digitalization

Until now, the benefits of digitalization within health care have been limited.

Many staff have blamed slow or outdated technology for adding to the administrative burden rather than alleviating it. For example, U.S. patient data was migrated to electronic health records (EHRs) in the early 2000s, but this data remains fragmented and reliant on manual inputs.

New telehealth services and digital care tools, like remote monitors, have had similar shortcomings, says Ashis Barad, MD, chief digital and technology officer at Hospital for Special Surgery (HSS), an academic medical center in New York that focuses on musculoskeletal health. Both technologies have helped improve access to health care by removing geographical barriers, he says, but they’ve failed to replicate the quality of in-person care or win trust from patients.

Agentic AI is different from these existing technologies, he insists.

Rather than relying on manual inputs or defaulting to human workers for any case that sits slightly outside a rigid framework, AI agents can handle nuanced, complex scenarios. They can make autonomous decisions, retrieve information from expert clinical sources, and iterate over time, freeing clinicians to focus on higher-level patient care. As Dr. Barad puts it: “Agentic AI takes your workflow and collapses it, augments it, supercharges it, and makes it more performant.”

At HSS, AI agents have already been deployed in multiple areas. They handle complex backend processes, such as insurance claims that previously took several weeks to complete and involved both HSS staff and a third-party contractor to handle the volume. Now, says Dr. Barad, AI agents complete 1,100 claims per month. They’ve reduced the appeals stage from 45 minutes to five and improved the success rate of those appeals from 65% to 100% in the nine months since implementation. HSS now handles all claims in-house.

Building on that success, HSS is now deploying AI agents in non-clinical patient-facing settings with an AI scheduling and triage service, as part of a collaboration with enterprise agentic AI developer Ema Unlimited. The service is accessible 24/7 via web, text, or phone. It uses conversational AI to ask patients clarifying questions about their condition and then books appointments with the most appropriate clinician, factoring in location, insurance coverage, and physician availability. “It completes the whole loop,” says Dr. Barad. The AI agent is trained on “all of our context, all of our rules, and all of our knowledge base,” he adds, providing patients with streamlined access to highly specialist knowledge from world-leading surgeons.

Given the high-stakes decisions delegated to AI agents, the triage service has built-in safeguards—sensitive, complex, or uncertain scenarios are escalated to human specialists. Every decision made by the AI agent is auditable and human staff can step in at any point. Patient data is kept secure and the system is trained on all HSS protocols, policies, and care pathways. By keeping humans in the loop, Ema says its technology strikes the balance between efficient automation, patient-first safety, and human-informed decision making.

As the technology becomes more prolific, it will be incumbent on providers to ensure they have these sorts of guardrails embedded into systems, says Dr. Barad. At HSS all decisions around the technology are filtered through an AI subcommittee that Dr. Barad co-chairs alongside a senior nursing executive. AI agents that may touch on patient care will be scrutinized with far more rigor than, say, backend processes, he explains.

AI agents prompt systems-level change

For example, Dr. Barad has plans to create a dedicated AI lab at the HSS main campus in New York City—a move that aims to democratize access to the technology across the organization. It will be open to all staff looking to understand or build AI agents, he explains, with informative classes and one-on-one training. “We’re getting agentic AI into everybody’s hands,” he says. This echoes research by Deloitte, which found that leading agentic AI adopters in health care were far more likely to have opted for multiagent solutions, redesigning end-to-end workflows rather than sticking to narrow solutions or individual use cases.

The key, it appears, is to integrate AI agents across the entire enterprise, treating them as a general-purpose technology. As Dr. Barad puts it: “It’s wrong to think of agentic AI in use cases… It’s a general-purpose technology, analogous to electricity.”

In practice, this means health-care providers need to set the right foundation to achieve value with agentic AI. This includes creating a unified data strategy, one that integrates fragmented data sources across an organization to create a single, comprehensive source of truth. In health care, data is often split across multiple departments and providers, each with their own legacy IT system.

In systems that rely on fragmented data sources, metrics often lack standardized definitions too. For example, Dr. Barad says that each hospital he’s worked in has had a slightly different definition for “time to start surgery,” a metric commonly used to gauge operating room efficiency. This level of fragmentation impedes AI agents from retrieving information from different sources or applications and assimilating the tacit knowledge that differentiates them from other technologies.

By creating greater interoperability of data at HSS, patient-facing AI agents can draw from a patient’s clinical care history and existing recommendations from their clinician, combine this information with current symptoms, and decide whether a situation requires escalation before notifying the correct specialist and informing the patient.

Building better outcomes

For Dr. Barad, the potential for AI agents to overhaul health care and alleviate the current pressures on resources, access, and patient care is huge.

He envisions a future in which 90% of non-clinical health-care tasks could be administered by AI agents, freeing clinicians up for what he calls white-glove work, meaning the most complex, specialized, and sensitive cases.

Most health-care providers seem equally optimistic. According to research by KPMG, 84% of providers are already comfortable handing decision making about specific processes over to AI agents.

“We’re spending so much time on keyboards and computers right now that we’re actually not doing what we should be doing,” says Dr. Barad. “This is going to rehumanize health care.”

This content was produced by Insights, the custom content arm of MIT Technology Review. It was not written by MIT Technology Review’s editorial staff. It was researched, designed, and written by human writers, editors, analysts, and illustrators. This includes the writing of surveys and collection of data for surveys. AI tools that may have been used were limited to secondary production processes that passed thorough human review.

Some of the forces that shape biopharma cluster development are constants year after year, such as the emergence of startups from university and research institute labs to develop new treatments, thanks to ideas backed by the brains of researchers and executives, and the bucks of serial entrepreneurs and other investors.

But in recent years, several additional unique circumstances have come to reshape how much and especially where biopharmas choose to grow, Matthew Gardner, CBRE Americas Life Sciences Leader, shared with GEN recently.

One is increased acquisition of lab and manufacturing properties by “mid-cap” biopharmas ranging between $2 billion and $10 billion in market capitalization (share price times the number of outstanding shares), as they seek to better control their supply chains by maintaining their own infrastructure in evolving from research- to commercialization-focused drug developers.

“They might have been more likely to lease in a different circumstance. They’ve definitely caught an opportunity to jump in and take ownership. That has been an ongoing trend, and that has been true coast-to-coast in most of the major centers,” Gardner said.

Among investor-owners, Gardner said, another transition has begun from pure-play biopharma real estate landlords to investors with broader portfolios encompassing healthcare—a reflection of how the two fields are increasingly converging. During December 2025 and January 2026, for example, the public real estate investment trust (REIT) Healthpeak shelled out $600 million to close on the acquisition of a 1.4-million square foot, 29-acre campus on Gateway Boulevard in South San Francisco, CA, from the nation’s largest biopharma REIT, Alexandria Real Estate Equities and BXP (formerly Boston Properties).

Those and other investors aim to cash in on the improving climate for biopharmas seeking to raise capital, from a recovering venture capital market to increased merger-and-acquisition (M&A) activity, and, in recent weeks, a revived market for initial public offerings (IPO).

Another key factor in recent cluster-building cited by Gardner is the “reshoring” of manufacturing in the U.S. by global biopharma giants, whether to satisfy growing demand for treatments—especially obesity drugs—or avoid tariffs, or both. While many of those new facilities are in manufacturing-heavy clusters like North Carolina and Greater Philadelphia, others have spread into Maryland and Virginia (the BioHealth Capital Region), and several new biomanufacturing sites have been built or are under construction in emerging clusters outside the Top 10—a trend GEN plans to explore in the coming weeks.

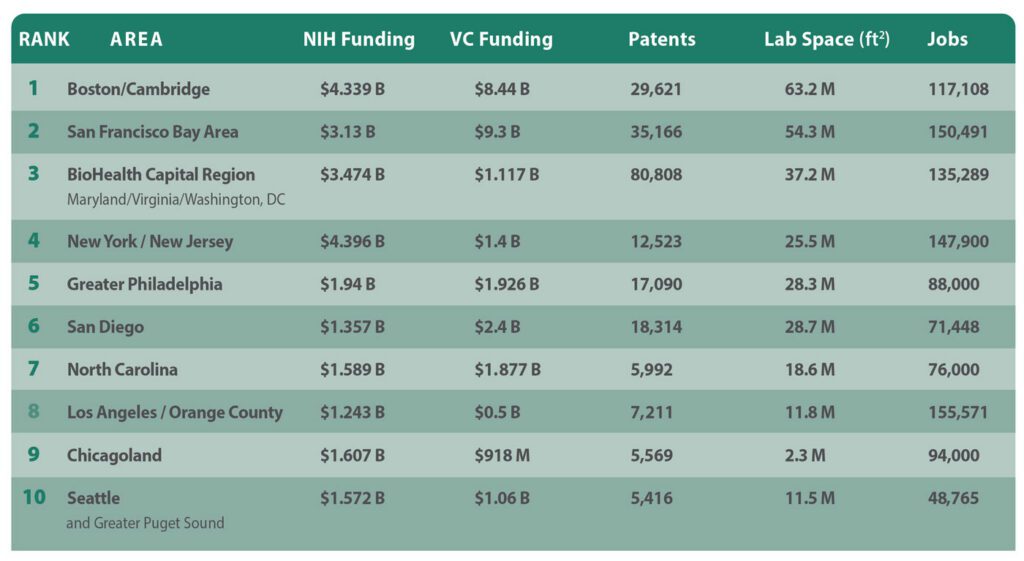

Speaking of top 10 clusters, GEN presents its latest edition of its nationally- and regionally-cited annual A-List of its top 10 U.S. biopharma cluster rankings, designed to show which regions are most competitive in attracting life sciences leaders, companies, and institutions. Over more than a decade, GEN has based its rankings on five criteria:

Patents: Figures from the Patent Public Search database of the U.S. Patent and Trademark Office, showing the number of patent families containing the word “biotechnology” and towns and cities within a given region or state.

NIH funding: Figures for NIH funding were taken from the publicly available NIH Research Portfolio Online Reporting Tools (RePORT) database for the current federal fiscal year through May 4, plus all of fiscal year 2025 (October 1, 2024, through September 30, 2025).

Venture capital funding: Figures for all of 2025 and the first quarter of 2026 as compiled by regional life sciences groups and PitchBook, which joins with the National Venture Capital Association to publish the quarterly Venture Monitor reports.

Laboratory space: The total-size-of-market figure, in millions of square feet, as furnished by regional life sciences groups. In regions that did not compile such information, the figure cited is the highest by any of several commercial real estate companies, including CBRE Group, Colliers, Cushman & Wakefield, JLL, and Newmark.

Number of jobs: The preferred sources for job figures were regional life sciences groups. Alternative sources included commercial real estate firms.

1. Boston/Cambridge, MA

Genentech has agreed to more than triple its space, growing from 30,000 to 100,000 square feet, within 1 Milestone Street at the Harvard University-owned, Tishman Speyer-developed Enterprise Research Campus in Boston’s Allston section [Breakthrough Properties, Studio Gang & Henning Larsen]

Years of growing into the nation’s top biopharma cluster have taken a toll on Boston and adjacent Cambridge, MA: The Wall Street Journal in December highlighted the inability of Boston-area PhDs to find work, while the region faces a glut of life sciences space as biopharmas and real estate developers scale back earlier plans—a 32.7% availability rate according to CBRE, up 70 basis points from Q1 2025. Takeda Pharmaceutical in March eliminated 247 jobs in Massachusetts, where the company has facilities in Lexington, MA, and Cambridge, part of a $1.3 billion restructuring that cut 634 jobs nationwide. Replimune in April chopped 223 jobs at its Woburn, MA, HQ, and Framingham, MA, manufacturing site after the FDA rejected its BLA seeking approval for RP1 [plus Bristol Myers Squibb’s Opdivo® (nivolumab)] for advanced melanoma. In February, Takeda placed 449,140 square feet within three Cambridge buildings on the sublease market, a week after Alexandria Real Estate Equities scrapped plans to convert 401 Park Drive in Boston’s Fenway section into lab space, with CEO and chief investment officer Peter M. Moglia saying the real estate investment trust was pivoting to meet growing demand for office space.

Among the region’s growing life-science companies: Genentech agreed to more than triple its space, growing from 30,000 to 100,000 square feet within One Milestone Street at the Harvard University-owned, Tishman Speyer-developed Enterprise Research Campus in Boston’s Allston section. Hemab Therapeutics (based in Cambridge and Copenhagen) and Seaport Therapeutics (Boston) both priced IPOs on April 30, raising $301.5 million and $254.88 million, respectively—a day after Avalyn Pharma (Boston) garnered $300 million in its IPO. In March, Terrestrial Bio became the first life-science tenant at Allston Labworks (250 Western Avenue) by leasing 42,000 square feet at the mixed-use building within Boston’s Allston neighborhood, while AI Proteins in January inked a 40,000-square-foot lease at 660 Commonwealth Avenue, within Related Beal’s One Kenmore Square in Boston. Regional companies finding buyers in April include Boston-based Kelonia Therapeutics and Cambridge-based Ajax Therapeutics, both to be acquired by Eli Lilly (for up to $7 billion and up to $2.3 billion, respectively) and Framingham-based KalVista Pharmaceuticals, to be acquired by Italy’s Chiesi Group for about $1.9 billion.

Boston/Cambridge enjoys the nation’s largest portfolio of lab space (63.2 million square feet according to industry group MassBio), but was bested by the San Francisco Bay Area in NIH funding (7,037 awards totaling $4.339 billion) following a year of government funding cuts. The region also placed second in VC ($6.85 billion in 2025, says MassBio; $1.59 billion in Q1 2026, according to PitchBook data cited by MassBio), but landed third in patents (29,621 families) and just fifth in jobs (117,108, according to MassBio).

2. San Francisco Bay Area

Eli Lilly Chair and CEO David A. Ricks and Nvidia Founder, president, and CEO Jensen Huang announce the companies’ five-year, $1 billion partnership to create a “Co-Innovation AI Lab” designed to address key challenges in AI drug discovery, announced on January 12 during the J.P. Morgan 44th Annual Healthcare Conference in San Francisco. The lab will be located within the Bay Area. [Nvidia]

Santa Clara, CA-based Nvidia and Eli Lilly electrified the annual J.P. Morgan Healthcare Conference, held in downtown San Francisco each January, by announcing a five-year, $1-billion collaboration to create a “Co-Innovation AI Lab” in the region to address key challenges in artificial intelligence (AI) drug discovery, powered by a supercomputer that went live in February. That welcome news aside, more than one-third of the region’s life-science space is available for lease (33.7% as of Q1, according to CBRE). And more space has entered the market: Pfizer confirmed plans in April to shut down its 164,000-square-foot research facility at 181 Oyster Point Blvd. in South San Francisco, CA, shifting employees to remote jobs. Cushman & Wakefield is marketing the space for sublease. Also, on the market in “South City” is a 21,552-square-foot lab building and surrounding 3.65 acres previously occupied by the U.S. Department of Agriculture, which is selling the building for just under $48 million. In May, Foster City, CA-based Gilead Sciences disclosed plans to lay off 108 employees based in Redwood City, CA, (and 84 in Rockville, MD) following its $7.8-billion acquisition of Arcellx.

Not all the recent news is bad: Gladstone Institutes plans early next year to open approximately 20 new labs employing about 300 scientists within the 105,000 square feet it agreed to lease in March at 1450 Owens Street, within Alexandria Real Estate Equities’ Alexandria Center® for Science and Technology–Mission Bay Megacampus. Natera inked a 62,969-square-foot lease at Brittan West in San Carlos, CA, in February. And last fall, Elon Musk’s Neuralink leased the entire approximately 144,000-square-foot 499 Forbes Boulevard in South San Francisco. On the financing side, SF-based Breakout Ventures in March closed its $114-million Fund III, which aims to invest in founder-led companies applying AI in biopharma, while Palo Alto, CA-based Surf Bio, whose lead investor for its only institutional round was Breakout, was acquired by San Diego-based Halozyme Therapeutics for up to $400 million, in a deal announced in January.

San Francisco and its suburbs topped Boston/Cambridge in VC ($7.8 billion in 2025, $1.5 billion in Q1 2026, both according to PitchBook). The Bay Area is second in three criteria: patents (35,166 families), lab space (54.3 million square feet according to Colliers), and jobs (150,491 according to BIOCOM California, but “more than 147,000” according to CBRE, both from last year). In NIH funding, the region is fourth (5,180 awards totaling $3.13 billion).

3. BioHealth Capital Region (Maryland, Virginia, and Washington, D.C.)

AstraZeneca has expanded the scope of its new manufacturing facility in Rivanna Futures, near Charlottesville, VA, into a $4.5 billion project designed to support manufacturing for weight management, metabolic, and cancer technologies, including antibody-drug conjugates. The project is expected to create 600 permanent jobs. [AstraZeneca]

The BHCR takes in Virginia and Maryland, both of which benefited over the past year from the domestic “reshoring” of biomanufacturing by pharma giants. AstraZeneca in November announced $2 billion in plans for Maryland that include a major expansion of its biologics manufacturing facility in Frederick, MD, and a new clinical manufacturing facility in Gaithersburg, MD. A month earlier, AstraZeneca expanded the scope of its new manufacturing facility in Rivanna Futures, near Charlottesville, VA, into a $4.5-billion project designed to support manufacturing for weight management, metabolic, and cancer technologies, including antibody-drug conjugates. The project is expected to create 600 permanent jobs. Also last fall, Merck & Co. broke ground on a $3 billion, 400,000-square-foot Center of Excellence for Pharmaceutical Manufacturing at its longstanding site in Elkton, VA, while Eli Lilly announced plans for a $5-billion manufacturing facility just west of Richmond, VA, in Goochland County that will be the company’s first-ever dedicated, fully integrated active pharmaceutical ingredient (API) and drug product facility for its bioconjugate platform and monoclonal antibody portfolio. However, a longtime strength of the region—the headquarters presence of the NIH and FDA—is now among its most serious challenges as government funding cuts chopped the workforces of both agencies last year by 3,500 and 1,200 jobs, respectively, though the FDA in recent months has worked to hire 1,000+ new staffers to fill reviewer, inspector, and investigator roles. And in May, Gilead Sciences disclosed plans to lay off 84 employees in Rockville, MD (and 108 in Redwood City, CA) following its $7.8-billion acquisition of Arcellx.

The BioHealth Capital Region fulfills its top-three cluster ambitions by continuing to lead the nation in patents (80,808 families) while placing third in NIH funding (4,665 awards totaling $3.474 billion) and lab space (37.208 million square feet according to JLL data cited by BHCR, including 9.2 million square feet of NIH labs in Bethesda, MD). The region is fourth in jobs (135,298, according to JLL and state data cited by BHCR), but seventh in venture capital ($1.117 billion in 2025, zero in Q1 2026, according to BHCR data).

4. New York/New Jersey

In New Jersey, New Brunswick’s Planning Board in February approved the $468 million H-3, the third phase of the HELIX downtown campus, a 40-story 554,000 square foot tower, for which the city council approved a 30-year PILOT agreement that will generate $1.8 million a year in annual payments in lieu of taxes [DEVCO New Brunswick Development Corp.]

The Big Apple will soon see a big biotech campus emerge, the $1.6 billion, 2-million-plus-square-foot Science Park and Research Campus (SPARC) Kips Bay, projected to create more than 15,000 jobs by combining life-science space with academic and public health facilities. Exterior demolition is scheduled for the third quarter, followed by construction next year. However, Johnson & Johnson has shifted operations of its JLABS@NYC incubator to site owner New York Genome Center, part of a corporate cutback of its incubator network. The 17-member Emerging Technology Advisory Board appointed by New York Gov. Kathy Hochul (D), who is seeking re-election this year, proposed numerous efforts in December to expand life sciences activity statewide, including a $65-million “Excellence” fund and a $40-million pre-commercialization fund. At deadline, the fate of those efforts was unknown despite a tentative agreement on May 7 of a $268-billion state budget.

In New Jersey, New Brunswick’s Planning Board in February approved the $468-million H-3, the third phase of the HELIX downtown campus, a 40-story, 554,000-square-foot tower, for which the city council approved a 30-year PILOT agreement that will generate $1.8 million a year in annual payments in lieu of taxes. In suburban Westchester County, Regeneron Pharmaceuticals is completing a $1.8-billion HQ expansion in Tarrytown but has scuttled earlier plans to expand across the Hudson River into the Rockland County village of Suffern, where the company spent $39 million to buy an old Avon Cosmetics warehouse for conversion into an infectious disease lab and a cold storage facility. In February, Regeneron hired JLL to market the site for sublease.

New York and its northern New Jersey suburbs lead the nation in NIH funding (7,033 awards totaling $4.396 billion) and are third in jobs (147,900, according to Cushman & Wakefield). From there, the region falls to the middle of the pack, placing fifth in VC ($1 billion in 2025 and about $400 million in Q1 2026, both according to PitchBook), and sixth in both lab space (25.5 million square feet, according to Colliers) and patents (12,523 families).

5. Greater Philadelphia

Eli Lilly made history in January by announcing Pennsylvania’s largest-ever biotech project, a $3.5 billion biomanufacturing site planned for Upper Macungie Township, an hour’s drive northwest of Philadelphia. Lilly plans to base 850 jobs at the plant, which will produce retatrutide and other weight loss drugs when it becomes operational in 2031. Lilly also has plans for Philadelphia, namely a 44,000-square-foot Lilly Gateway Labs innovation hub in Center City West at 2300 Market set to open later this year. [Eli Lilly]

Eli Lilly made history in January by announcing Pennsylvania’s largest-ever biotech project, a $3.5-billion biomanufacturing site planned for Upper Macungie Township, an hour’s drive northwest of Philadelphia. Lilly plans to base 850 jobs at the plant, which will produce retatrutide and other weight loss drugs when it becomes operational in 2031. Lilly also has plans for the City of Brotherly Love, namely a 44,000-square-foot Lilly Gateway Labs innovation hub in Center City West at 2300 Market set to open later this year. And, in Philadelphia’s Old City, Thermo Fisher Scientific last November opened its East Coast Advanced Therapies Collaboration Center (ATxCC) within the BioLabs for Advanced Therapeutics incubator.

Thermo Fisher Scientific executives last November celebrated the opening of the biotech tools giant’s East Coast Advanced Therapies Collaboration Center (ATxCC) in Philadelphia’s Old City, within the BioLabs for Advanced Therapeutics incubator. [Thermo Fisher Scientific]

The region’s rich biotech history includes the first gene therapy Luxturna® marketed by Roche-owned Spark Therapeutics—which is completing its $575 million Gene Therapy Innovation Center in University City despite laying off more than half of its Philly staff last year. In March, TerraPower Isotopes announced plans for a $450-million radioisotope manufacturing facility designed to produce actinium-225 for cancer treatments. The project will employ 225, receive $10 million in state grants, and rise within The Bellwether District, the 1,300-acre former Philadelphia Energy Solutions refinery site. Greater Philadelphia has long benefited from innovations from its institutions, two of which won more than $100 million in NIH funding during the 2025 federal fiscal year, the Perelman School of Medicine at the University of Pennsylvania to Children’s Hospital of Philadelphia (CHOP)—which last year treated KJ Muldoon (“Baby KJ”), the world’s first patient to receive a personalized CRISPR gene-editing therapy (for CPS1 deficiency). The region’s needs for more C-suite talent and venture capital remain persistent challenges to cluster growth, stakeholders told The Philadelphia Inquirer in December, though Audrey Greenberg, chair of corporate development and “Mayo Venture Partner” at Mayo Clinic and founder of AG Capital Advisors, told the Inquirer: “I’m going to be starting my companies all here in Philadelphia, because that’s where I am.”

Greater Philadelphia improved the most this year, climbing two positions in this year’s A-List after remaining fifth in patents (17,090 families) and rising to fifth in lab space (25.9 million square feet, according to Colliers’ data cited by Pennsylvania’s Department of Economic Development or DECD) and NIH funding (3,201 awards totaling $1.94 billion). The region jumped four spots to fifth in VC ($1.31 billion in 2025, $616 million in Q1 2026, says Colliers), but dipped to seventh in jobs (88,000, also according to DECD), including nearly 10,000 with cell and gene therapy expertise.

6. San Diego

Novartis broke ground in February on a $1.1 billion, 466,000-square-foot global Biomedical Research center in San Diego, expected to house 1,000 employees when operational in 2029, three months after opening a radioligand therapy manufacturing facility for cancer treatments in Carlsbad, CA. [Novartis]

The Biotechnology Innovation Organization (BIO) expects to draw 20,000 to its BIO International Convention when it returns this month to the San Diego Convention Center. The region remains a vibrant life-sciences cluster: Novartis broke ground in February on a $1.1-billion, 466,000-square-foot global Biomedical Research center in San Diego, expected to house 1,000 employees when operational in 2029, three months after opening a radioligand therapy manufacturing facility for cancer treatments in Carlsbad, CA. Eli Lilly in March completed its $1.2-billion acquisition of home-grown Ventyx Biosciences—months after the pharma opened a Lilly Gateway Labs innovation hub with Alexandria Real Estate Equities in Torrey Pines. The J. Craig Venter Institute—whose founder died April 29 at age 79—plans this summer to move its West Coast headquarters from the University of California San Diego campus in La Jolla to the downtown Research and Development District (RaDD), a $1.6-billion, 1.7-million-square-foot campus on the city’s Pacific coastline completed last year by San Diego-based developer IQHQ—which is fighting an investor’s fraud allegations related to a $50-million investment in 2020. Home-grown F5 Therapeutics (up to 10 employees) folded in March, while two other San Diego biotechs laid off employees this year: Gossamer Bio (65 employees, nearly half its workforce, as of May 15, following a Phase III trial failure) and BioAlta (70% of its staff, which was 41 as of December 31, 2025). In February, San Diego drug developer Iambic Therapeutics inked an up-to-$1.7-billion collaboration with Takeda Pharmaceutical, which will use Iambic’s AI technologies and wet lab capabilities to design and develop small molecule drugs. And global contract development and manufacturing organization (CDMO) Bora Biologics, in January, opened a $30-million expanded manufacturing facility with two to four 2,000-liter bioreactors, corresponding seed trains, and advanced downstream processing equipment.

“America’s Finest City” and vicinity stayed third in VC ($1.9 billion in 2025, says PitchBook, $743 million in Q1 2026 according to a GEN spot-check of recent deals) and fourth in patents (18,314 families) but dipped to fifth in lab space (28.685 million square feet, according to CBRE). While the San Diego region last year rose to ninth in NIH funding (2,001 awards totaling $1.357 billion), it slid to ninth in jobs (71,448, according to year-old BIOCOM California data).

7. North Carolina

Roche’s Genentech subsidiary in January expanded to $2 billion its planned investment in its first East Coast manufacturing facility in Holly Springs, NC, which broke ground last year and is set to support 500+ manufacturing jobs when operational by 2029. [Genentech]

Always strong on drug manufacturing, North Carolina is among the biggest beneficiaries of biopharma’s reshoring push. In April, AbbVie announced a $1.4-billion, 185-acre drug production facility in Durham County near Research Triangle Park (RTP), expected to employ 734. Roche’s Genentech subsidiary in January expanded to $2 billion its planned investment in its first East Coast manufacturing facility in Holly Springs, NC, which broke ground last year and is set to support 500+ manufacturing jobs when operational by 2029. And in November 2025, Novartis said it will expand Tar Heel State operations into a flagship manufacturing hub by adding capabilities for sterile filling of biologics into syringes and vials at its current Durham site, constructing two new Durham facilities for manufacturing biologics and sterile packaging, and building a new Morrisville, NC, site to produce solid dosage tablets and capsules, including packaging. Morrisville is where Novartis also plans to build a 56,200-square-foot facility focused on API manufacturing for solid dosage tablets, capsules, and RNA therapeutics, a project announced April 30. Manufacturing sites account for most of the combined $24.5 billion in new or expanded facilities with a potential 15,000+ new jobs that life sciences companies have announced statewide since 2021, according to the state-funded North Carolina Biotechnology Center. As for startups, Raleigh-based Slate Medicines launched in February with $130 million in Series A financing to fund development of therapies led by its migraine candidate, the anti-PACAP monoclonal antibody SLTE-1009 licensed from Zhongshan, China-based DartsBio Pharmaceuticals, and set to start Phase I trials in mid-2026.

The Tar Heel State climbed to fourth in VC ($1.6 billion in 2025, $276.8 million in Q1 2026, both according to the state-funded North Carolina Biotechnology Center). But North Carolina showed consistency on the other criteria, ranking seventh in NIH funding (2,248 awards totaling $1.589 billion) and lab space (18.6 million square feet, according to JLL), and eighth in jobs (76,000, says the Center) and patents (5,992 families).

8. Los Angeles / Orange County, CA

Amgen executives mark the groundbreaking for the biotech giant’s $600 million center for science and innovation being built within its Thousand Oaks, CA, headquarters campus, set to integrate Research & Development and Process Development teams to smoothen the transition from drug discovery to commercial manufacturing. [Amgen]

The region’s biopharma anchor Amgen broke ground last fall on a $600-million center for science and innovation being built within its Thousand Oaks, CA, headquarters campus, set to integrate research & development and process development teams to smooth the transition from drug discovery to commercial manufacturing. “With the first shovel in the ground, we’re reaffirming something essential: We discover here, we manufacture here, we deliver for patients from Thousand Oaks to all around the world,” Amgen chairman and CEO Robert A. Bradway said. Regional industry group BioscienceLA CEO Stephanie Hsieh recently acknowledged the region’s fragmentation as a challenge—from 88 cities in LA County alone, to the numerous county, city, and private agencies focused on growing the bioindustry— while citing strengths such as corporate anchors Amgen, Takeda Pharmaceutical, and Gilead Sciences-owned Kite Pharma, plus institutions like USC, UCLA, Cedars-Sinai, and City of Hope.

California signaled interest in growing the region’s biopharma industry last August when the state-funded California Jobs First Regional Investment Initiative awarded $23.92 million to a coalition led by Los Angeles County’s Department of Economic Opportunity (DEO) toward four programs intended to create 10,000 jobs by 2030. Most of the money ($19 million) was approved for a DEO revolving loan fund to support startups, especially those looking to graduate from the Larta Institute’s commercialization and capital access accelerator into lab space within Los Angeles County. Larta was awarded $3.3 million to expand its Heal.LA Bioscience & Healthcare Accelerator and assist small startups via its Larta Impact Fund, a revolving loan fund.

Los Angeles/ Orange County would still lead the nation in jobs, based on a year-old BIOCOM California tally of 155,571, which also includes San Bernardino and Ventura counties; figures run as low as 116,000, compiled last year for the four counties plus Riverside and Santa Barbara counties (regional industry group SoCalBio). The region finished seventh in patents (7,211 families), eighth in lab space (11.7 million square feet, according to JLL), and 10th in both NIH funding (1,911 awards totaling $1.243 billion) and VC ($500 million in 2025, zero in Q1 2026, according to PitchBook).

9. Chicagoland

AbbVie plans to build two new active pharmaceutical ingredient (API) manufacturing facilities totaling $380 million at its campus in North Chicago, IL, where the biopharma giant is headquartered. [AbbVie]

At least one developer has pivoted to a large non-biotech tenant to help fill a Chicago campus once envisioned as a life-sciences mecca: Trammell Crow in March inked a $100-million, 169,860-square-foot lease with candy/chocolate giant Mars to base 600 jobs at 400 North Aberdeen Street within the Fulton Market campus. Other biotech spaces are in the works: In North Chicago, Rosalind Franklin University of Medicine and Science plans to nearly double the size of its Helix 51 biomedical incubator to just under 13,000 square feet by adding 6,000 square feet of new lab and office space, citing growing demand from early-stage biotechs. The expansion is expected to create space for up to 10 additional companies. Also in North Chicago, home-grown AbbVie announced plans to build two new API manufacturing facilities totaling $380 million at its campus in the Chicago suburb. The facilities—designed to support production of next-generation neuroscience and obesity treatments—are set to be fully operational in 2029. However, AbbVie opted to build its planned $1.4-billion biomanufacturing campus not in North Chicago but 821 miles southeast in Durham, NC. Across Illinois, biotech stakeholders have applauded Gov. J.B. Pritzker (D) for proposing to sweeten the state’s Research & Development Tax Credit program by allowing companies to transfer their credits for cash. “This is a transformative step for our startup and growth-stage ecosystem,” stated John Conrad, president and CEO of the Illinois Biotechnology Innovation Organization (iBIO). Pritzker is seeking a third term in November vs. Darren Bailey (R).

The Windy City and vicinity rank sixth in both NIH funding (2,658 awards totaling $1.607 billion) and jobs (94,000, according to statewide industry group Illinois Biotechnology Innovation Organization or iBIO). The region places ninth in patents (5,569 families) and VC ($917.677 million in 2025, says iBIO, zero in Q1 2026,

10. Seattle

AGC Biologics, a global CDMO, expanded its regional research footprint last fall by signing a 37,575-square-foot lease at Element Research Center in Bothell, WA. [AGC Biologics]

Seattle and the Greater Puget Sound’s strong base of academic and other nonprofit research institutions helped the region achieve consecutive years of Nobel laureates: Mary E. Brunkow, PhD, of the Institute for Systems Biology in Seattle co-won the 2025 prize in Physiology or Medicine a year after David Baker, PhD, director of the Institute for Protein Design at University of Washington (UW), co-won the 2024 prize in Chemistry. A UW spinout, Seattle-based 3D tissue model developer Curi Bio, closed in December on a $10-million Series B financing led by South Korean contract research organization DreamCIS. In April, Achieve Life Sciences (based in Seattle and Vancouver, BC) announced an up-to-$354 million private placement whose purposes include funding a Phase III trial and future commercialization of e-cigarette cessation candidate cytisinicline, while Athira Pharma landed up to $236 million in conjunction with acquiring exclusive rights from Sermonix Pharmaceuticals to the Phase III metastatic breast cancer candidate lasofoxifene. AGC Biologics, a global CDMO, expanded its regional research footprint last fall by signing a 37,575-square-foot lease at Element Research Center in Bothell, WA. However, Astellas Pharma told Washington state officials in April it will shutter the Seattle site of its Universal Cells subsidiary by 2028, with 50 employees to be impacted via layoffs or transfers to South San Francisco, CA, or Westborough, MA.

Seattle and its suburbs placed highest at eighth in both NIH funding (eighth with 1,892 awards totaling $1.572 billion) and VC ($1.06 billion in 2025, zero in Q1 2026, according to industry group Life Science Washington). The region was ninth in lab space (11.46 million square feet, according to regional real estate firm Flinn Ferguson Cresa) and 10th in both jobs (48,765 according to Life Science Washington) and patents (5,416 families).

Biotech is producing scientific breakthroughs that once seemed impossible. But according to longtime industry executive Jeremy Levin, the institutions that support these advances, from regulators, to investors, and even public trust in science itself — are beginning to fracture.

Levin is the founder and chairman of Ovid Therapeutics and former CEO of Teva Pharmaceuticals. In his new book, “Biotech in the Balance: Saving a Strategic Industry in an Age of Distrust,” he argues that political upheaval, weakening institutions, short-term investing, and more are putting the future of the industry at risk, even though the science itself continues to accelerate.

On this week’s episode of “The Readout Loud,” Levin advocates for federal changes that could incentivize biotech investment, and for pharmaceutical companies, in particular, to call out how regulatory upheaval is harming the drug industry. “When an institution such as this, which is critical, is shaken, the industry must stand firm. It must call out why this is a problem. … The titans are dead silent right now,” he said.

Below are highlights from his conversation with hosts Elaine Chen, Adam Feuerstein, and Allison DeAngelis.

This transcript of the interview has been lightly edited for length and clarity.

Background: Telemonitoring has been shown to improve glycemic control in type 2 diabetes, but the optimal design for effectively integrating self-management education remains unclear. Including patient feedback in the design process can enhance usability, increase engagement, and improve the feasibility and effectiveness of the intervention in real-world settings. Objective: This study aims to explore participants’ experiences and the acceptability of 2 different telemonitoring intervention designs and trial procedures used in a feasibility trial among people with non–insulin-dependent type 2 diabetes. Methods: Using a qualitative research design, semistructured interviews were conducted with participants who had completed the telemonitoring intervention. The interviews were analyzed using the thematic approach outlined by Braun and Clarke. Results: A total of 12 participants were interviewed. Four major themes emerged from the analysis: (1) acceptance of and experience with telemonitoring and devices, (2) structure and flow of the intervention, (3) relationship with and support from health care professionals, and (4) learning to live with diabetes. Participants found the devices easy to use, particularly self-monitoring of blood glucose, which was perceived as highly relevant and informative. Technical challenges were primarily related to the activity tracker and initial device setup. The measurement schedule supported self-management, though some participants found it inflexible and difficult to integrate into daily life. Continuous communication with health care professionals was highly valued and fostered trust. Participants reported increased insight into the relationship between lifestyle behaviors and blood glucose levels, which motivated healthier dietary choices and increased physical activity. Participants described that telemonitoring enhanced their understanding of diabetes and supported their engagement in self-management, although preferences for measurement types and frequency varied. Conclusions: Participants reported overall satisfaction, attributing it to structured monitoring and consultations with health care professionals that supported self-management. Blood glucose, physical activity, and diet were considered the most relevant data types. Tailoring the intervention to user priorities and improving the usability of devices and the intervention structure may increase engagement and motivation. Integrating continuous glucose monitoring may further reduce the burden associated with self-monitoring in future telemonitoring interventions for people with type 2 diabetes.

<img src="https://jmir-production.s3.us-east-2.amazonaws.com/thumbs/4e2fd6df650361b283a095fb5985d81f" />

As health security expands to address climate, trust, and systemic risks, a continued focus on emergency preparedness risks fragmenting public health and obscuring the political and economic drivers of those risks.